Four out of ten audits are dead on arrival and do not have sufficient audit evidence to support the audit opinion; the prognosis is even worse if you’re not a Big 4 firm! This statement sounds alarming, but it is accurate based on our in-depth analysis of the PCAOB inspection reports of annually inspected firms over the past six years. We believe it is good practice for all firms, regardless of size, to analyze the audit deficiencies detailed in PCAOB inspection reports, improve their audit training, and make necessary improvements to their audit procedures.

The nine annually inspected firms included in our analysis are:

- Deloitte & Touche LLP

- PricewaterhouseCoopers LLP

- Ernst & Young LLP

- KPMG LLP

- McGladrey LLP

- Grant Thornton LLP

- BDO USA, LLP

- Crowe Horwath LLP

- MaloneBailey, LLP

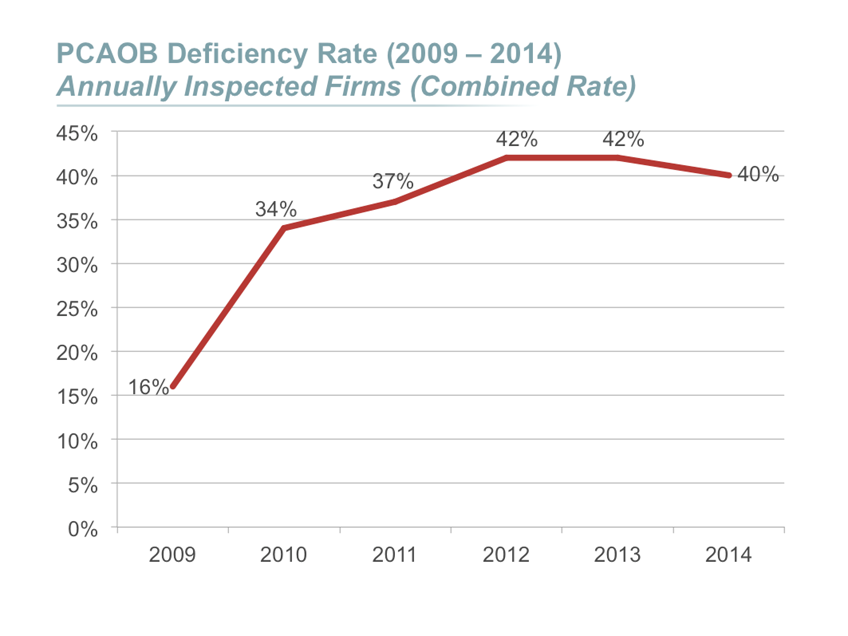

Based on inspections by the PCAOB of audits performed in 2014, the annually inspected firms had a combined audit deficiency rate of 40%. Of the 281 audits inspected, 111 audits had at least one audit deficiency noted by the PCAOB. However, the audit deficiency rate for individual firms varied widely, from a low of 21% (great job, Deloitte & Touche LLP!) to a high of 74%!

While the combined audit deficiency rate is down slightly from the audit deficiency rates noted in the previous two years (42%), it’s still higher than the PCAOB would like to see.

Note: As of the date of this post, the PCAOB inspection report on the 2014 audits of Grant Thornton LLP had not yet been released to the public and, as a result, the 2014 statistics do not include the firm.

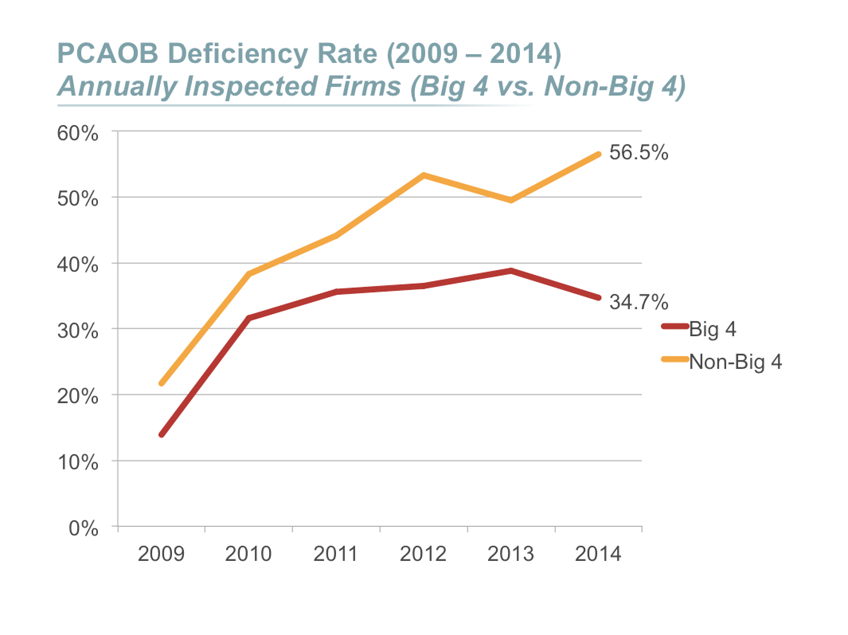

There is a huge difference in the audit deficiency rates of the Big 4 firms (Deloitte, PwC, EY, and KPMG) compared to the other annually inspected firms, and the gap appears to be widening!

All of the firms have the same quality of people working on their audit engagements. They graduated from the same universities and qualified as CPAs at similar rates. Why then the difference in audit deficiency rates? We believe it comes down to the investment in quality training programs.

Big 4 firms spend MILLIONS of dollars on internal training for their professionals and issue tons of thought leadership publications. We know because we are lucky to be a training partner with one of these firms! They have massive Learning and Development (L&D) teams providing national, regional, and local trainings. And they bring in outside help for their training, to improve its quality and provide it in a more timely manner. (The other annually inspected firms spend a fraction of that. We know because we train them too!)

Bottom line: These other firms need to improve their audit training, especially if they want to compete with the Big 4.

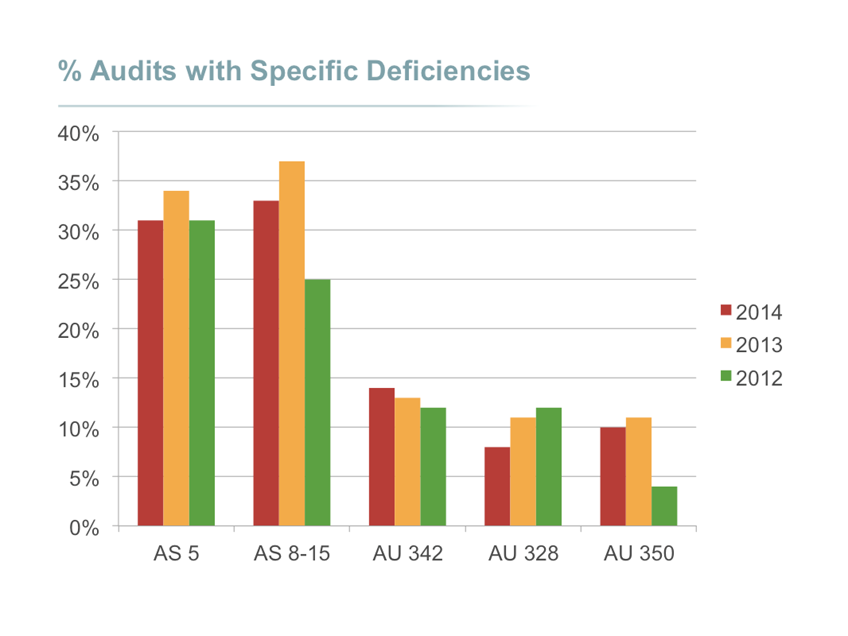

The vast majority of the audit deficiencies noted in inspections over the past three years were in the following five areas:

- Auditing internal control over financial reporting (AS 5)

- Assessing and responding to risks of material misstatement (AS 8-15)

- Auditing accounting estimates (AU 342)

- Auditing fair value measurements and disclosures (AU 328)

- Performing audit sampling procedures (AU 350)

As we discuss in this post, the PCAOB has released preliminary results of their inspections of 2015 audits. The main areas of deficiencies remain unchanged, but there is good news: the PCAOB noted a decrease in the overall number of audit deficiencies based on their inspections of the annually inspected firms. However, inspections staff observed an overall high number of audit deficiencies for triennially inspected firms.

We’ve helped a Big 4 firm navigate PCAOB inspection findings, and we can help you too! We’ve developed a course, Preparing for PCAOB Audits and Inspections, to assist you in navigating the complexities of the PCAOB inspection process. We can facilitate the course at your location, or you can license a complete set of course materials for your own professionals to instruct the course in-house. Contact us today to learn more.

Want more information on the results of our analysis of PCAOB inspection reports? You’re in luck! We’re set to release our first ever eBook in the coming weeks to help auditors:

- Learn from findings in recent PCAOB inspection reports,

- Improve their audit training,

- Prevent recurring audit deficiencies, and

- Strengthen the quality of their audits.

Stay tuned!

Comments (0)

Add a Comment