Accounting for Impairment under ASC 360

ASC 360 governs the accounting for long-lived assets, which are required to be evaluated for impairment. And anytime you are dealing with impairment, you know it will involve significant estimates and judgment, making the accounting complex! This post explores how to properly determine if an impairment loss exists for a long-lived asset and, if so, how to properly measure it in accordance with ASC 360.

When to test for impairment under ASC 360

So, when do long-lived assets, such as property, plant and equipment (PP&E) need to be tested for impairment? Per ASC 360, “a long-lived asset should be tested for recoverability whenever events or changes in circumstances indicate that its carrying amount may not be recoverable.” What this quote is trying to say, is that a long-lived asset should be tested for impairment upon the occurrence of a triggering event.

What constitutes a triggering event?

Are triggering events only caused by changes in conditions internal to the company? Or can they be caused by events external to the company? What about changes in circumstances? The answer is “all of the above!” ASC 360 lists several examples of triggering events, such as:

- A significant decrease in the market price of a long-lived asset;

- A change in the way an asset or asset group is being used or a change in its physical condition;

- An adverse change in legal factors, regulation, or business environment;

- Past, current, or expected cash flow losses associated with the asset or asset group; or

- An expectation that the asset will be disposed of significantly before the end of its useful life.

While the list provided by ASC 360 is a great start, remember that this is not an all-inclusive list! There are many other events or changes in circumstances that may be indicative of a triggering event. Identifying a triggering event is not as straightforward as it may seem and involves significant judgment.

What level to test for impairment under ASC 360

Once a triggering event has occurred, a company must determine the appropriate level to test for impairment (i.e., the unit of account to test). Typically, long-lived assets are either tested at the individual asset level, or at the asset group level. ASC 360 states that the test should be performed “at the lowest level for which identifiable cash flows are largely independent of the cash flows of other assets and liabilities.”

This generally means the impairment test will be performed at the asset group level for long-lived assets, as it would be less common to determine the cash flows associated with an individual asset. This tends to be an area heavily scrutinized by regulators as companies prefer to group assets at the highest level possible (because it’s less likely to have impairment!).

Keep in mind, when testing an asset group for impairment, the carrying amounts of ALL assets and liabilities included in the asset group should have already been tested for impairment (and should reflect any impairment recognized).

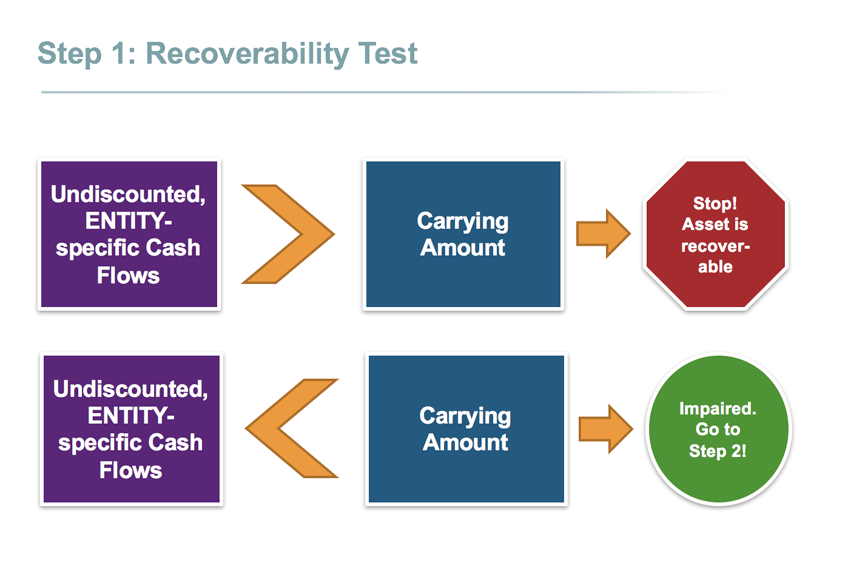

Step 1: The recoverability test

ASC 360 provides guidance on a two-step impairment test. Step 1 is often referred to as the recoverability test (i.e., can the company recover the carrying amount of the asset or asset group through its intended use)?

Step 1 begins with the undiscounted, entity-specific cash flows, which are the sum of the future undiscounted cash flows expected to be derived from the use of the asset. The company compares this amount to the carrying value of the asset or asset group in question. The carrying value is simply the amount on the company’s books at the date of the test. If the undiscounted cash flows exceed the carrying amount, the company should be able to recover the carrying value through its use of the asset (i.e., there is no impairment). If, however, the undiscounted cash flows do not exceed the carrying value, then the company must proceed to Step 2.

Step 2: Measure the impairment

A company measures the impairment amount in Step 2, which is calculated by comparing the fair value of the asset or asset group to its carrying value. If the fair value is less than the carrying value, the difference is booked as an impairment charge in the income statement, and the offsetting side of the entry writes down the asset or asset group in the balance sheet to its fair value.

For more on determining fair value, check out our course collection on fair value measurements!

Don’t forget about ASC 360 disclosures!

Even if the asset or asset group is currently not impaired, if there has been a triggering event or if the asset group is close to failing Step 1 of the impairment test, the SEC expects registrants to disclose that information to investors as well as the potential amount of impairment (if it is reasonably estimable)! The SEC never wants to be surprised by an impairment charge!

For more information on impairment testing of long-lived assets, check out our PP&E and Intangible Assets impairment course or visit our Impairment of Nonfinancial Assets topic page!

About GAAP Dynamics

We’re a DIFFERENT type of accounting training firm. We view training as an opportunity to empower professionals to make informed decisions at the right time. Whether it’s U.S. GAAP, IFRS, or audit training, we’ve trained thousands of professionals since 2001, including at some of the world’s largest firms. Our promise: Accurate, relevant, engaging, and fun training. Want to know how GAAP Dynamics can help you? Let’s talk!

Disclaimer

This post is for informational purposes only and should not be relied upon as official accounting guidance. While we’ve ensured accuracy as of the publishing date, standards evolve. Please consult a professional for specific advice.