The 2017 AICPA Conference was bustling with excitement regarding changes to the auditor’s report which were approved by the SEC on October 24, 2017. These changes, most of which are included within AS 3101: The Auditor’s Report on an Audit of Financial Statements When the Auditor Expresses and Unqualified Opinion, provide more information to investors and represent the first significant changes to the auditor’s reporting model in more than 70 years. According to PCAOB Chairman James Doty, “It will make the auditor’s report more relevant, useful, and informative to investors and other financial statement users. The new standard will breathe new life into a formulaic reporting model.”

The auditor’s report will continue to provide a “pass/fail” opinion, but, beginning with audits for fiscal years ending on or after December 15, 2017, the auditor’s report will now contain clarifications regarding independence, auditor responsibilities, and communication of an auditor’s continuous years of service to the company. As a result, the standardized language of the report has been changed and now includes the addition of the phrase “whether to error or fraud,” in describing the auditor’s responsibilities under PCAOB auditing standard.

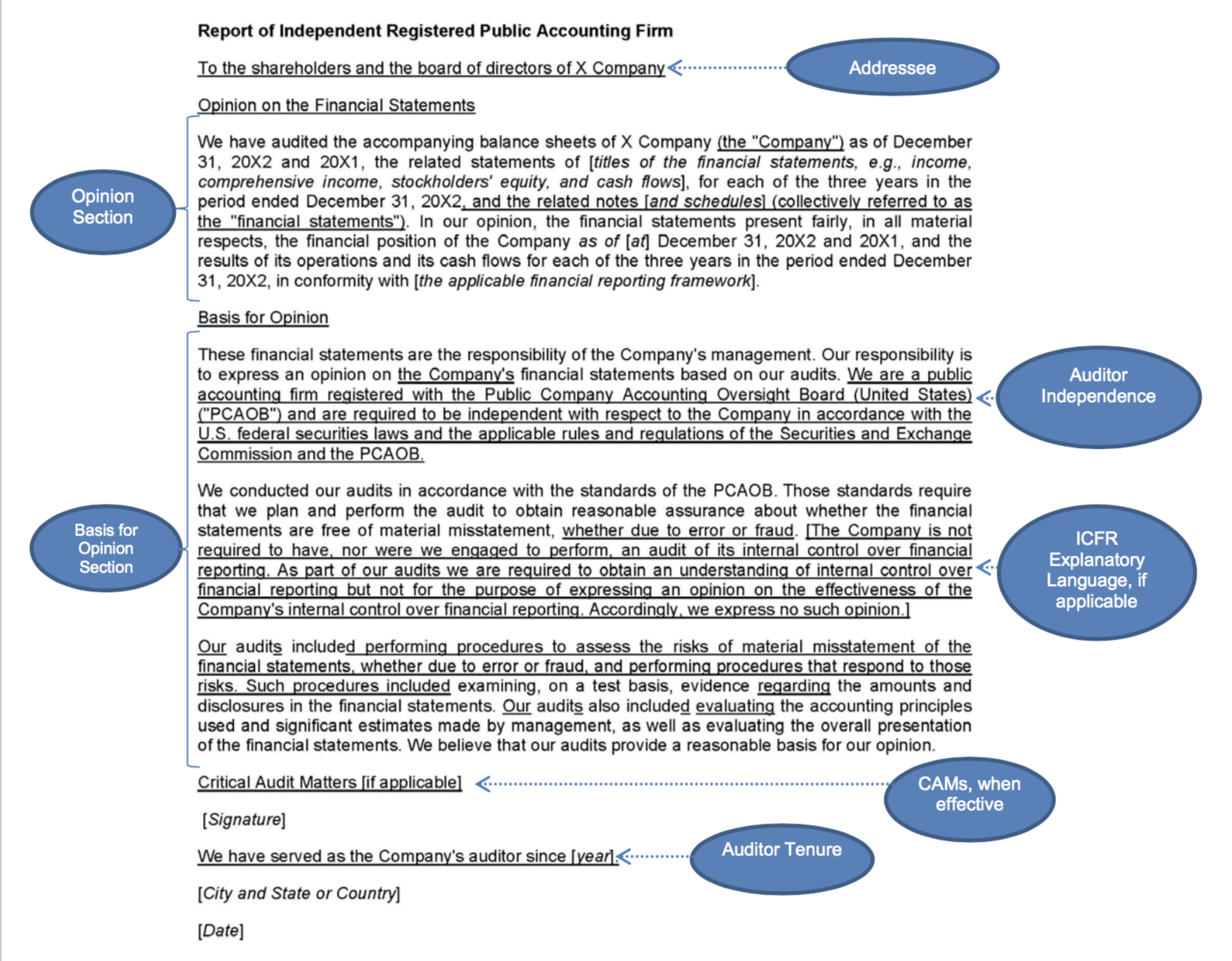

However, probably the most significant change, is the requirement for auditors to disclose critical audit matters (CAMs). CAMs are defined under AS 3101 as matters arising from the audit of financial statements that:

- Have been communicated or were required to be communicated to the audit committee;

- Relate to accounts or disclosures that are material to the financial statements; and

- Involve especially challenging, subjective, or complex auditor judgment.

Disclosure of CAMs is not required for audits of emerging growth companies, brokers and dealers, employee stock plans, or investment funds. If no CAMs are noted during the audit, this fact needs to be noted within the auditor’s report.

With respect to disclosing the CAMs, the PCAOB has set staggered effective dates. For audits of large accelerated filers, the new requirements are effective for fiscal years ending on or after June 30, 2019, while the effective date for audits of all other companies is fiscal years ending on or after December 15, 2020.

Wesley Bricker, Chief Accountant, Office of the Chief Accountant, had some good advice for auditors when implementing the new rules. He suggested that this year end they communicate with the audit committee things like:

- What would the credit audit matters be this year?

- What would be the close calls?

- When could those matters have been raised, and which ones could have been identified at the start of the audit cycle?

- What does the auditor expect to say about those matters?

- When would we expect to see a draft report or at least a draft of the critical audit matters?

Looking for more guidance? Well, you’re in luck! On December 4, the PCAOB published staff guidance on implementing the new changes. The guidance addresses key changes to the auditor’s report required this year, such as:

- The form of the auditor’s report,

- Disclosure of audit tenure,

- A statement on auditor independence, and

- A required explanatory paragraph on Internal Control Over Financial Reporting (ICFR) in certain circumstances.

It also provides an annotated example of the new auditor’s report (with the new language underlined):

“This guidance was prepared to help firms as they implement the first phase of changes to the auditor’s report,” said Martin F. Baumann, PCAOB Chief Auditor and Director of Professional Standards.

Mr. Baumann stated, “These changes will improve the relevance and usefulness of the auditor’s report by providing additional information to investors.” According to SEC Commissioner Kara Stein, the new auditor’s report “will improve the investor’s experience.” However, not everyone is so optimistic. SEC Chairman Jay Clayton warned that he will be disappointed if, trying to fend off frivolous lawsuits, the disclosure of critical audit matters results in “boilerplate” disclosures. Only time will tell.

I’m excited about seeing examples of the new auditor’s report, including the critical audit matters. Are you? Give us your feedback.

Disclaimer

This post is published to spread the love of GAAP and provided for informational purposes only. Although we are CPAs and have made every effort to ensure the factual accuracy of the post as of the date it was published, we are not responsible for your ultimate compliance with accounting or auditing standards and you agree not to hold us responsible for such. In addition, we take no responsibility for updating old posts, but may do so from time to time.

Comments (0)

Add a Comment