Overview of Accounting for Investments in Equity Securities (ASC 321)

Creating an eLearning course is a labor of love. Well, I must really love what I do as I just spent the past two weeks drafting a storyboard for a new course for the GAAP Dynamics Learning Library. This course covers the accounting for investments in equity securities in accordance with ASC 321. You can check out the course here. Since I am deep into the topic, I wanted to share the love in this post.

The accounting for equity securities and related ownership interests dramatically changed as a result of the issuance of ASU 2016-01 Recognition and Measurement of Financial Assets and Financial Liabilities. In fact, it created an entirely new topic within the FASB Codification – ASC Topic 321 Investments – Equity Securities (ASC 321).

Remember the trading and available-for-sale categories for equity securities? They’re gone! What about the headache of determining whether impairment of such investments was other than temporary? That’s gone too!

Why? Because ASC 321 requires equity investments with readily determinable fair values within its scope to be measured at fair value with changes in fair value recognized in net income, making these categories and other-than-temporary impairment assessments moot.

But not all investments are within the scope of ASC 321. Is yours? Let’s find out!

Scope of ASC 321, Investments – Equity Securities

Does specialized industry guidance apply?

First, if the investor is subject to specialized accounting guidance, such as those applicable to broker-dealers, defined benefit pension plans, and investment companies, ASC 321 doesn’t apply. Why? Because such entities account for substantially all of their investments at fair value with changes in fair value reported in earnings.

Is the investment an equity security or other ownership interest?

Second, ASC 321 only applies to investments in equity securities and other ownership interests in an entity. These “other ownership interests” include investments in partnerships, unincorporated joint venture, and limited liability companies. If the investment doesn’t meet the definition of an equity security, then it is most likely that it is a debt security subject to ASC 320, which has been Vicky’s labor of love over the past 2 weeks!

Does the investment meet one of the scope exceptions set out in ASC 321?

Third, there are certain scope exceptions outlined in ASC 321-10-15-5. The guidance in ASC 321 does not apply to any of the following:

- Derivative instruments within the scope of ASC 815

- Investments accounted for under the equity method

- Investments in consolidated subsidiaries

- Exchange memberships

- Federal Home Loan Bank and Federal Reserve Bank Stock

Now that we know ASC 321 applies, we have to know the answers to several questions in order to determine the appropriate accounting.

Accounting for investments in equity securities

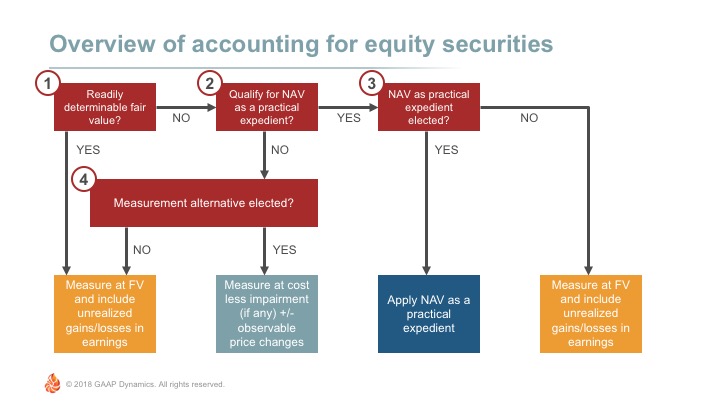

Does the investment have a readily determinable fair value?

According to ASC 321, an equity security has a readily determinable fair value if it meets any of the following conditions:

- The fair value of an equity security is readily determinable if sales prices or bid-and-asked quotations are currently available on a securities exchange registered with the U.S. Securities and Exchange Commission (SEC) or in an over-the-counter market, provided that those prices or quotations for the over-the-counter market are publicly reported by the National Association of Securities Dealers Automated Quotations (NASDAQ) systems or by the OTC Markets Group Inc. Restricted stock meets that definition if the restriction terminates within one year.

- The fair value of an equity security traded only in a foreign market is readily determinable if that foreign market is of a breadth and scope comparable to one of the U.S. markets referred to above.

- The fair value of an equity security that is an investment in a mutual fund or in a structure similar to a mutual fund (that is, a limited partnership or a venture capital entity) is readily determinable if the fair value per share (unit) is determined and published and is the basis for current transactions.

If the investment has a readily determinable fair value, then it must be reported on the balance sheet at fair value with changes in fair value reported in the income statement. However, if the investment does not have a readily determinable fair value, then we need to go to the next question.

Does the investment qualify for use of net asset value (NAV) as a practical expedient?

- In order to quality for use of NAV as a practical expedient to fair value, all of the following criteria need to be met:

- The investment does not have a readily determinable fair value;

- The investment is in an investment company within the scope of ASC 946; and

- The NAV is calculated in a manner consistent with the measurement principles of ASC 946 as of the reporting entity’s measurement date.

If the entity does not qualify for use of NAV as a practical expedient, then we can skip to the last question. However, if the entity does qualify for use of NAV as a practical expedient, then we need to determine if the entity actually elects to use it.

Does the entity intend to use NAV as a practical expedient?

Assuming they qualify, the use of NAV as a practical expedient to fair value is an accounting policy election made by entities. If they intend to use this election, then they should measure the investment at NAV each period. However, if they choose not to apply NAV as a practical expedient, then the investment must be reported on the balance sheet at fair value with changes in fair value reported in the income statement.

Is the measurement alternative elected?

If an investment does not have a readily determinable fair value and it does not qualify for use of NAV as a practical expedient, then the entity may elect to utilize a new measurement alternative prescribed by ASC 321. Under the measurement alternative, the investment is measured at cost minus impairment, if any, plus or minus changes from observable price changes in orderly transactions for the identical or a similar investment of the same issuer.

The measurement alternative is an accounting policy election, meaning it is not required. Entities are always permitted to account for the investment at fair value with changes in fair value reported in earnings.

Closing thoughts

I hope this post has helped you understand the new accounting for investment in equity securities under ASC 321. Admittedly, there’s much more to this topic, including the details of applying the measurement alternative, but we’re saving that for another post. Stay tuned! If you do don’t want to wait, check out our Investments: Equity Securities eLearning course and start learning now!

About GAAP Dynamics

We’re a DIFFERENT type of accounting training firm. We view training as an opportunity to empower professionals to make informed decisions at the right time. Whether it’s U.S. GAAP, IFRS, or audit training, we’ve trained thousands of professionals since 2001, including at some of the world’s largest firms. Our promise: Accurate, relevant, engaging, and fun training. Want to know how GAAP Dynamics can help you? Let’s talk!

Disclaimer

This post is for informational purposes only and should not be relied upon as official accounting guidance. While we’ve ensured accuracy as of the publishing date, standards evolve. Please consult a professional for specific advice.