Derivative and Hedge Accounting: An Overview of ASC 815

What comes to mind when you hear the word derivative? Or, how about hedge accounting?

If you feel intimidated or cringe at the thought of accounting for derivatives and hedging activities, you are not alone!

A long time ago, I was offered a job with a large financial institution to become a subject matter expert on derivative and hedge accounting. I was definitely nervous (and maybe a bit unqualified). As I look back on this job, I am glad I took it. While there were definitely challenges and a fair amount of frustration with fully grasping the rules of ASC 815, I’ve come out on the other side (I find derivative and hedge strategies fascinating!).

When learners shy away from ASC 815, I tend to reassure them that the guidance is not as complicated as it seems! I often pose the question:

How do you eat an elephant?

Well, one bite at a time, of course! And, that is my advice for tackling derivative and hedge accounting.

Derivative and hedge accounting training

We offer a four-part training series on the accounting for derivatives and hedging. Our collection breaks down the monstrous topic of ASC 815 into more manageable chunks and summaries the complex lingo, concepts, and rules in a more easily understandable manner through the use of examples, video, interactivity, and mini case questions.

The remainder of this post provides an introduction to derivatives and hedging and gives an overview on each of our courses.

Accounting for derivatives and hedging activity

ASC 815 requires a derivative to be recorded on the balance sheet as an asset or liability and to be measured at fair value. Changes in fair value each period are reported in earnings, unless the derivative is designated in a qualifying hedge relationship.

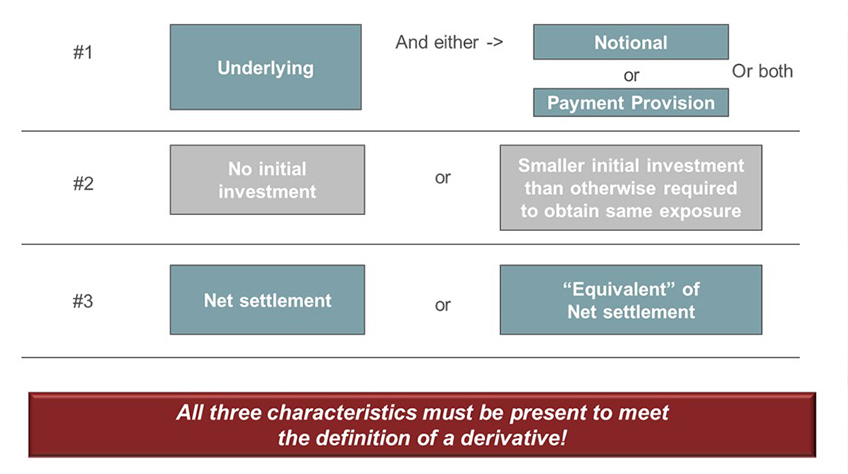

In order to apply the accounting, it’s important that you know what a derivative is. ASC 815 provides a characteristics-based definition of a derivative. There are three characteristics, all of which must be present in order to meet the definition of a derivative and be accounted for as such. The image below depicts a summary of the three characteristics.

Course 1 – Derivatives: Characteristics and Scope Exceptions

The three characteristics of a derivative are covered in detail as understanding the characteristics-based definition is critical to applying the accounting guidance. Note that contracts do exist where the three characteristics may be met, but ASC 815 provides an exclusion from the scope of derivative accounting. Scope exceptions to the guidance are also reviewed in this course.

In addition to the characteristics and scope exceptions, this course discusses the basic derivative concepts which include terminology and detailed explanations of common derivative types. Examples are provided to illustrate application of the characteristic-based definition to these common derivative instruments.

Course 2 – Derivatives: Embedded Derivatives

The accounting for derivatives also applies to derivatives that are embedded in other contracts.

There are contracts, referred to as hybrid instruments, that do not in their entirety meet the definition of a derivative but may have terms within the overall contract that affect some or all of the cash flows or the value of other exchanges required by the contract in a manner similar to a derivative instrument. The issue with these types of contracts is determining whether it should remain as one instrument for valuation and accounting purposes or whether the embedded derivative must be accounted for separately from the host contract. The rules to make that determination are covered in depth this this course.

As mentioned above, there is special accounting treatment when a derivative is designated in a qualifying hedge accounting relationship. The accounting depends upon the type of hedging relationship. The last two courses in our four-part series are dedicated to hedge accounting.

Course 3 – Hedge Accounting: Introduction to Hedge Accounting

This course discusses the difference between economic hedging and hedge accounting, the different types of hedging strategies, and the accounting for these qualifying hedges. The three hedging strategies are:

- Fair value hedging: A hedge of the exposure to changes in the fair value of a recognized asset or liability, or of an unrecognized firm commitment, which are attributable to a particular risk

- Cash flow hedging: A hedge of the exposure to variability in the cash flows of a recognized asset or liability, or of a forecasted transaction, that is attributable to a particular risk

- Net investment hedging: A hedge of the foreign currency exposure of a net investment in a foreign operation

Course 4 – Hedge Accounting: Hedge Accounting Qualification

Hedge accounting is a choice! Therefore, ASC 815 mandates strict criteria that must be met in order to apply “special” hedge accounting. This course covers the criteria to qualify for hedge accounting and the requirements to maintain hedge qualification to be able to continue applying the special hedge accounting.

The requirements can be categorized as follows:

- Documentation requirements

- Requirements for hedge items and the risk being hedged

- Requirements for the hedging instrument, and

- Effectiveness requirements

Concluding thoughts

There is a lot to learn about derivatives, hedging, and the accounting for these transactions under ASC 815. And while it may feel daunting at first, our training series is available to easily digest these complex topics, and to make it more manageable to build a solid foundational knowledge. Additionally, check out our Derivatives and Hedging topic page for more information.

About GAAP Dynamics

We’re a DIFFERENT type of accounting training firm. We view training as an opportunity to empower professionals to make informed decisions at the right time. Whether it’s U.S. GAAP, IFRS, or audit training, we’ve trained thousands of professionals since 2001, including at some of the world’s largest firms. Our promise: Accurate, relevant, engaging, and fun training. Want to know how GAAP Dynamics can help you? Let’s talk!

Disclaimer

This post is for informational purposes only and should not be relied upon as official accounting guidance. While we’ve ensured accuracy as of the publishing date, standards evolve. Please consult a professional for specific advice.