Investment Management

Accounting resources for ASC 946

Investment management is an umbrella term for an industry that includes various funds, such as hedge funds, mutual funds, private equity funds, and many others (collectively referred to as “investment companies” under U.S. GAAP). As it relates to accounting, the investment management industry is special. The business activities and the needs of the readers of the financial statements are unique compared to other industries. As a result, U.S. GAAP has special accounting and reporting principles solely for this industry contained in ASC 946, Financial Services – Investment Companies.

Despite the industry-specific guidance, the investment management industry is constantly evolving and innovating investment products, strategies, and structures, resulting in the need to apply judgment and interpretation of the accounting principles to ensure financial statements are prepared properly. As a result of years of experience working in the industry and training professionals about the accounting and reporting for investment management, GAAP Dynamics has developed expertise in this area. Below, we share our insights about key accounting issues, key differences between U.S. GAAP and IFRS, and useful resources for learning more about the investment management industry.

Welcome video

Accounting issues

As noted above, the investment management industry is special. Therefore, the primary accounting issues impacting the industry are not necessarily those that a typical entity would identify. U.S. GAAP includes an entire topic dedicated to accounting principles for investment companies, ASC 946. However, absent specific principles in ASC 946, other U.S. GAAP topics must also be applied (e.g., ASC 820 (Fair Value Measurements) and ASC 740 (Income Taxes)), resulting in a challenge to navigate the principles of U.S. GAAP for the industry. However, many prefer this challenge to the challenge in IFRS that requires the application of largely general accounting principles being applied to an industry with unique transactions and reporting considerations.

Definition of investment company

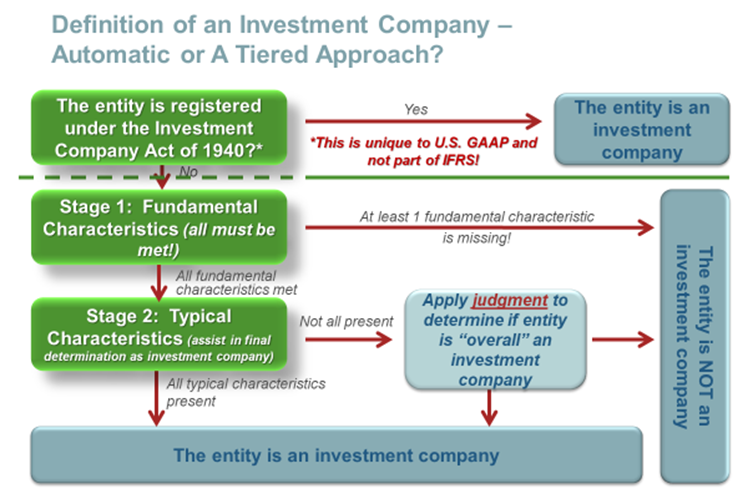

Before we get too involved in the special aspects of accounting and reporting for funds, the first issue to address is whether or not a fund is worthy of receiving this special treatment.

ASC 946 not only provides industry-specific accounting and reporting requirements for funds, it also defines an investment company and the types of entities that are subject to these special principles.

Qualification as an investment company may be achieved either automatically, by being registered under the SEC’s Investment Company Act of 1940, or by meeting the definition of an investment company.

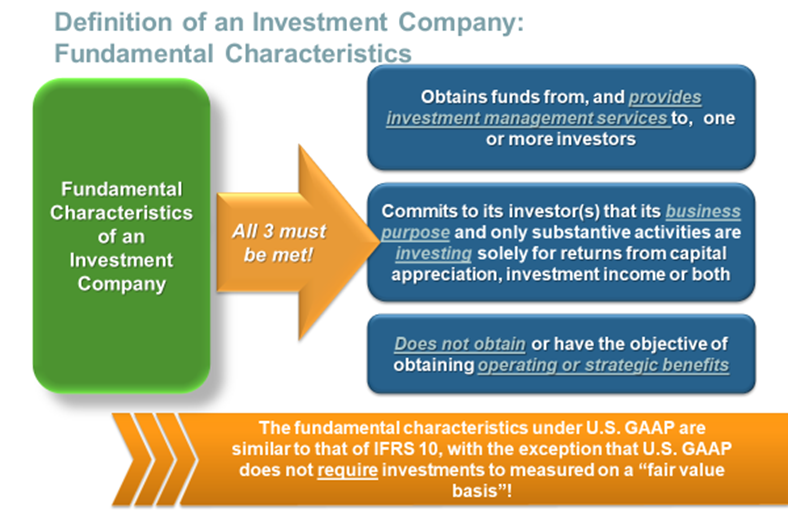

The definition of an investment company includes consideration of both fundamental and typical characteristics. The fundamental characteristics are mandatory and must be present in order for the entity to be considered an investment company.

Typical characteristics are those that are not mandatory but would generally be expected. Typical characteristics of an investment company include:

- It has more than one investment, to diversify the risk portfolio and maximize returns;

- It has multiple investors, who pool their funds to maximize investment opportunities;

- It has investors that are not related parties of the entity;

- It has ownership interests in the form of equity or similar interests;

- Management of substantially all investments on a fair value basis

If the entity does not have all of the typical characteristics, it must apply judgment, using overall facts and circumstances, to determine if the entity meets the definition of an investment company.

While many funds will clearly meet the definition of an investment company, others may not meet the definition so clearly. Specifically, private equity funds and real estate funds, that are more actively involved in their investments through management, development, and operations, often require careful consideration of ASC 946 when making this determination.

Accounting for and measuring investments

Once it’s clear the fund is an investment company, the biggest issue, without question, will be how to account for and measure the investments held by the fund. And while the accounting principles are quite straight-forward, the application of these principles is a challenge.

ASC 946 requires that all investments be measured at fair value, with changes in fair value recognized through the income statement. “All” investments include those held in debt and equity instruments, as well as alternative investments, such as derivatives, investments in other funds (e.g., fund of funds), and non-financial investments (e.g., real estate, collectibles, cryptocurrencies, etc.). The extent of ownership also does not change this principle. For example, regardless of whether an investment company holds a 40% or 80% stake in an equity investment, ASC 946 requires the investment to be accounted for at fair value and NOT by using the equity method of accounting or consolidation. The reason for this principle has to do with the needs of the users of the financial statements (e.g., investors and future investors), where the fair value of the funds’ portfolio is the most useful information to present.

As a result, fair value becomes a very important measurement basis for an investment company. And while investment companies commonly use this measurement basis, they do so by applying ASC 820, not the industry-specific guidance in ASC 946.

While the determination of fair value may be easy for marketable investments in debt and equity securities, many funds may hold hard-to-value investments that do not have a readily determinable fair value. Investments in private equity, non-traditional debt, and alternative investments may require significant judgment when estimating fair value. Luckily, there is plenty of help to assist in these judgments, from online training to interpretive guides issued by the Big 4, which we cover in the resources section below.

One common issue faced by investment companies is how to measure investments in other investment companies, such as when the fund is a fund-of-funds. ASC 820 allows an entity to elect to measure fair value using net asset value (NAV) as a practical expedient to fair value, which greatly simplifies the measurement of these investments. However, it may only be elected if certain conditions are met.

Once fair value has been mastered, the challenges continue under ASC 946. Depending on the type of investment held, there are many other unique accounting requirements for investment companies, including:

- Accounting for transaction costs

- Distinguishing a distribution from an equity investment as a return “of” capital versus a return “on” capital

- Recognition of dividend income on the ex-dividend date

- Presentation of interest income on debt securities separately from other changes in fair value using the effective rate method

- Recognition and measurement of foreign currency movements in foreign investments

- Accounting for controlling interests in other investment companies

Service provider fees

From an operational perspective, investment companies are relatively lean and simple entities and therefore have very few, if any, employees. In fact, the everyday activities undertaken by the fund are generally provided by outside service providers, resulting in a number of service provider fees being charged to the fund and/or its investors. Typical service providers may include:

- Investment manager/ adviser/ general partner – manages investment portfolio

- Distributor – responsible for the selling of fund shares to investors

- Administrator – provides recordkeeping and accounting services

- Transfer Agent – tracks and manages investor shares (e.g., purchases and distributions)

- Custodian – holds investments held by the fund

- Legal Counsel – provides legal services

- Independent public accountant – audits fund’s financial statements

The investment manager is a critical service provider. Not only do they typically receive the largest fees from the fund, but they are most often the creator of the fund in the first place. Investment managers often establish funds in order to provide services to it!

Fees paid to service providers, particularly the investment manager, is an area where the investment management industry starts to really show its unique qualities. Fee structures often include a performance-based component and may require complex calculations to determine amounts owed, often resulting in material amounts. Terminology, such as hurdle rates, high-water marks, waterfalls, carried interest (or carry), and clawbacks, further add to the complexity of this area. ASC 946 requires both base and performance fees to be measured and accrued on interim dates by a fund based on the actual performance through the accrual date. As a result, it is important to understand the fee structures to ensure they are properly calculated each reporting period.

Further complication may arise when dealing with funds structured as limited partnerships where the general partner is the investment manager. In these arrangements, management fees may be paid through a reallocation of capital rather than a cash payment. In these instances, judgment may need to be applied as to whether such reallocations are to be recognized in the income statement (as a non-owner-related service) or within shareholders’ equity (as an owner-related transaction).

Other arrangements commonly exist between a fund and its service providers that result in accounting and reporting consequences such as:

- Expense limitation arrangements

- Expense offset or reimbursement arrangements

Complex capital structures

Investment companies are often set up as limited partnerships but may also be established as corporations. This structure is often dictated by tax law and local regulations where the fund has been established.

Funds also have unique capital structures that are not typically seen in other industries. The structures vary widely and continue to evolve. Some of the most common structures include:

The multi-class structure:

The multi-class structure is most commonly found in mutual funds and creates multiple classes of shares in which investors may invest. The different share classes allow for different types of investors (e.g., institutional versus individual) and provide flexibility with regards to how distribution fees will be assessed for each class (e.g., front-end load, back-end load, 12b-1/ level load, or no distribution fee at all). However, the multi-class structure may also be used for other purposes, such as providing classes for investment in different currencies or geographical locations.

The master-feeder structure:

In the master-feeder structure, investments are held in a separate master fund. Investors invest in various feeder funds, which use investor proceeds to invest in the master fund. While this structure may seem unnecessarily complicated, its primary purpose is tax optimization. By segregating investor groups and establishing funds in tax-exempt, off-shore locales, the fund manager is able to pool tax-exempt investors with investors that are subject to taxation to invest in the same investment portfolio, without disrupting the tax status of either group of investors.

The fund of funds (FoF) structure:

A fund of funds (FoF) is exactly what it sounds like…a fund that holds investments almost exclusively in other funds. The attraction to these types of investments is two-fold: diversification (even more than an individual fund can offer!) and accessibility of investments. FoFs are common with hedge funds as these mainly private funds require a rather large minimum investment for investors (which ensures the fund can maintain a minimum number of investors and maintain private fund status, while also maximizing its net assets under management). A FoF will pool investor funds to ensure that minimum investment can be made and allow investors to gain access to these types of investments.

Each of these structures, although unique, have a common purpose: to maximize the investment in a particular fund by providing investors with advantages and the accessibility they are seeking. Whether it is the cost structure, tax optimization, diversification, or access to investment, the capital structure of a fund can open the door to more investors!

However, with these complex structures come potential accounting and reporting issues. From an accounting perspective, the mix of “shared” fund activities and “isolated” capital pools result in the need to perform allocations of expenses, earnings, and distributions to each of the capital groups. This gets complicated, especially when units in a fund are regularly being bought and sold. For financial reporting, ASC 946 contains a number of specific presentation and disclosure requirements, some of which are unique to specific capital structures. Therefore, care must be given to comply with these requirements depending on the structure of the fund.

Financial statement presentation

The final, and perhaps most identifiable accounting issue for investment management is the financial statement presentation requirements for funds. The financial statements just plain look different!

Not only are the names different, with statements like the “Statement of Operations” or “Statement of Assets and Liabilities”, but there are also additional schedules and information not seen in typical industries. Also, a Statement of Cash Flows may or may not be presented depending on whether certain criteria are met.

Some of the most noticeable differences, other than nomenclature, is the inclusion of the following items and schedules:

- Net asset value (NAV) and NAV per share – This statistic represents the value of the fund for investors, and in the case of NAV per share, the value of each share at the reporting date. ASC 946 requires these amounts be included in the Statement of Assets and Liabilities or Statement of Net Asset (whichever is provided by the fund), and by class of investors.

- Schedule of Investments (SOI) – This is typically a separate schedule in the financial statements (although for registered funds, it may be included as part of the Statement of Net Assets) and reports the investment portfolio of the fund. ASC 946 contains specific rules, often complex, regarding its presentation and when investments must be reported separately from other investments. There are also unique reporting requirements for registered vs. unregistered/ private funds.

- Financial Highlights (FiHis) – The FiHis are either presented as a separate schedule in the financial statements or within the footnote disclosures and represent the key performance indicators (KPIs) of the fund. FiHis can be broken down into the following categories:

- Per share data (e.g., investment income/loss, realized/unrealized gains or losses, distributions to shareholders, capital items, etc.)

- Ratios (e.g., expenses to average net assets and investment income to average net assets)

- Total return (or internal rate of return for certain funds)

- Turnover (only applicable to registered funds)

ASC 946 has very prescriptive rules regarding the information to be presented and how it is to be calculated, therefore, care should be taken when preparing the FiHis.

The purpose and importance of these unique schedules and disclosures is quite obvious as this information is of utmost importance to an investor trying to determine whether they want to invest (or continue to invest) in a particular fund. Therefore, focus is often on these unique presentation items by auditors, regulators, and investors.

Accounting differences: ASC 946 vs. IFRS

U.S. GAAP’s ASC 946 Financial Services – Investment Companies contains industry-specific accounting and reporting guidance for investment companies (the U.S. GAAP for funds), while IFRS has only limited industry-specific guidance in the form of a few scope exceptions. It should be noted that ASC 946 is to be used in conjunction with the other topic sections of U.S. GAAP. However, this leads to many potential differences between U.S. GAAP and IFRS, some more significant and common than others. Below we focus only on what we consider some of the most significant differences commonly encountered by funds.

| U.S. GAAP | IFRS | |

|---|---|---|

| Industry-specific guidance | ||

| Industry-specific guidance for investment companies | ASC 946 Financial Services – Investment Companies contains industry-specific accounting and reporting guidance for funds. | No industry specific guidance provided other than scope exceptions in IFRS 10, Consolidated Financial Statements and IAS 28, Investments in Associates and Joint Ventures. |

| Specific reporting requirements for registered investment companies | ASC 946 includes specific presentation requirements for registered (i.e., SEC-regulated) funds that are sometimes different from those requirements for private funds. | IFRS does not distinguish between the reporting and presentation requirements of regulated vs. private funds. |

| Definition of an investment company | ||

| ASC 946 defines an “investment company” and if a fund meets this definition, it is subject to the industry-specific principles in ASC 946. If this definition is not met, these principles do not apply and the entity must apply U.S. GAAP for typical industries. | IFRS 10 defines an “investment entity” and if a fund meets this definition, it is scoped out of the consolidation guidance within IFRS 10 only. This definition, while similar to U.S. GAAP, requires that investments be managed and evaluated on a fair value basis (whereas this is only a “typical characteristic” under U.S. GAAP). | |

| Fair value measurement | ||

| NAV as a practical expedient to fair value | ASC 820 provides a practical expedient for measuring certain investments in other funds at NAV, instead of applying the fair value definition if certain conditions are met. | IFRS 13 does not provide a similar practical expedient and therefore, investments in other funds must be measured at fair value. |

| Investments | ||

| Measurement of investments held by an investment company | ASC 946 requires ALL investments, other than investments in other investment companies, to be measured at fair value, with changes in fair value through earnings. This includes both financial and non-financial investments. | IFRS does not have similar industry-specific guidance and therefore each investment’s accounting and measurement is dictated by the relevant IFRS standard. This means financial instruments would apply IFRS 9 and determine the proper categorization of accounting, and non-financial investments would apply other relevant standards, such as IAS 40 (for investment property), IAS 38 (for intangible assets, such as cryptocurrencies), etc. |

| Recognition and presentation of interest income | Interest income earned on debt securities must be presented in the Statement of Operations apart from other changes in fair value (i.e., unrealized or realized gains or losses). | Interest earned on debt securities accounted for at fair value through profit or loss (FVTPL) are not required to separately recognize interest income in the Statement of Comprehensive Income. |

| Presentation of expenses | ||

| Presentation of expense limitations, reimbursements, and offsets | ASC 946 specifically requires a “gross” presentation of expense limitation, reimbursement, and offset arrangements between the fund and its service providers. As a result, the impact prior to consideration of the arrangements is presented in the Statement of Operations, with the offsetting impact of the arrangements captured as a reduction of total expenses (presented under the “Total Expenses” line item). | IFRS does not have similar presentation guidance and therefore, the effects of these arrangements may be presented on a net basis under IFRS. |

| Classification of debt versus equity | ||

| Puttable shares | U.S. GAAP’s debt versus equity classification rules are more “form over substance”, resulting in shares that are puttable (such as those issued by open-end funds) to be classified within shareholders’ equity (i.e., net assets). | IAS 32, Financial Instruments: Presentation, defines a financial liability as an obligation to deliver cash. Puttable shares generally will meet the definition of a financial liability, unless a narrow scope exception related to puttable shares is met and allows for presentation in shareholders’ equity. If puttable shares are liability-classified, distributions and remeasurements are required to be captured in the income statement as interest expense. |

| Financial statements | ||

| Primary financial statements | U.S. GAAP has unique names for each of its primary financial statements, including: – Statement of assets and liabilities (or Statement of net assets for certain registered investment companies) – Statement of operations – Statement of changes in net assets – Statement of cash flows | IFRS does not have unique financial statements for investment entities and therefore, the requirements in IAS 1/ IFRS 18 apply. |

| Schedule of investments | U.S. GAAP requires an investment company to prepare and present a Schedule of Investments (SOI) as part of its financial statements. The presentation requirements of the SOI are explicit in ASC 946. | While some form of investment schedule is often included in IFRS financial statements of a fund, it is not a required item under IAS 1/ IFRS 18 and therefore, diversity exists in practice surrounding how a schedule is prepared, if at all. |

| Financial highlights | U.S. GAAP requires investment companies to include financial highlights (FiHis) as a separate schedule of the financial statements or within the footnotes. The reporting requirements for FiHis are quite specific and detailed within ASC 946. | IFRS does not require specific financial highlights other than what would be required from its general disclosure requirements. Therefore, there is diversity in practice as to how these key performance indicators are prepared and presented. |

| Statement of cash flows | U.S. GAAP does not require a Statement of cash flows to be presented by an investment company if certain criteria are met. | IFRS requires a Statement of cash flows for funds without exception under IAS 7. |

For more comprehensive coverage of differences between the two accounting frameworks, refer to the thought leadership provided by the Big 4 accounting firms. See the Accounting Resources section below for links. Additionally, GAAP Dynamics offers a “GAAP Differences” course that can be facilitated via webinar or in-person – contact us for details.

Online learning

Due to the specialized nature of the investment management industry, CPE eligible accounting training specific to investment companies and funds is practically non-existent! GAAP Dynamics recognized this void and designed a comprehensive training program, our Investment Management Industry Fundamentals Collection. This collection is in addition to our full library of U.S. GAAP and IFRS eLearning courses which can be found on our online eLearning platform, the GAAP Dynamics Learning Library. Our courses are continually updated and new courses are constantly being added, so check back often!

Investment Management: Industry Overview – Part of the “Investment Management Industry Fundamentals” course collection, this CPE-eligible, eLearning course (1.0 CPE) provide you with an overview of the investment management industry and an introduction to the applicable accounting guidance for investment companies in accordance with U.S. GAAP (ASC 946). As you tour the investment company landscape, the following topics will be discussed: characteristics of an investment company, investment strategies, general categories, capital and legal structures, key players (service providers), definition of an investment company in U.S. GAAP, overview of applicable U.S. GAAP accounting guidance. This online course also explores the fundamental differences between U.S. GAAP and IFRS related to investment company accounting. This course is a must for anyone beginning to work in the investment management industry and serves as the starting point for our online Investment Management Industry Fundamentals course collection.

Investment Management: Investments – Part of the “Investment Management Industry Fundamentals” course collection, this CPE-eligible, eLearning course (2.0 CPE) begins with an overview of typical investments held by investment companies. This online course then takes a deeper dive into the accounting and reporting requirements for investments in equity securities, debt securities, and alternative investments. With the investments line item being so important to entities in the investment management industry, this course is a must for accountants in this industry!

Fair Value: Overview of ASC 820 – Do you realize that fair value is one of the most widespread financial concepts in U.S. GAAP? As such, this course is a must for any accountant or auditor! After a review of the various balance sheet items which utilize fair value measurements, this CPE-eligible, eLearning course (1.5 CPE) explores key concepts of fair value including: Utilizing market participant assumptions, distinguishing between orderly transactions versus forced transactions, using exit prices and not entry prices, and determining the principal market. This online course then discusses the various approaches to determine fair value measurements, including the importance of inputs and their classification within the fair value hierarchy. The course concludes with a look at “real-life” fair value disclosures, highlighting the disclosure requirements within ASC 820.

Fair value: Advanced Issues – Now that you have a good understanding of fair value accounting in accordance with ASC 820 Fair Value Measurements, it’s time to take you knowledge to the next level! The second course in our Fair Value Measurement series, this CPE-eligible, eLearning course (1.5 CPE) dives into advanced fair value measurement issues. Level up your fair value measurement accounting knowledge with advanced topics such as distinguishing, active, inactive and disorderly markets, using net asset value (NAV) as a practical expedient to fair value, and considerations when determining the fair value of liabilities. This online course is a must for any accounting, but especially those responsible for financial reporting or auditing financial institutions.

Investment Management: Transactions with Service Providers – Part of the “Investment Management Industry Fundamentals” course collection, this CPE-eligible, eLearning course (1.5 CPE) explains who the typical service providers of an investment company are and how they are compensated, highlighting the fact that most of the functions of an investment company are performed by these service providers. Typical fee arrangements are covered in this online course, with particular focus on the accounting for management fees and distribution fees. Fee waiver, reimbursement, and expense offset arrangements are also discussed along with their presentation in the U.S. GAAP financial statements.

Investment Management: Transactions with Unit Holders – Part of the “Investment Management Industry Fundamentals” course collection, this CPE-eligible, eLearning course (1.5 CPE) describes how capital share transactions are accounted for by an investment company in accordance with U.S. GAAP, along with the accounting for other fees incurred by unit holders related to capital share transactions. In addition, this online course explores the common capital structures utilized by investment companies, including the key impacts those structures have on the U.S. GAAP financial statements.

Investment Management: Financial Reporting – Part of the “Investment Management Industry Fundamentals” course collection, this CPE-eligible, eLearning course (1.0 CPE) explains the financial reporting requirements for investment companies under U.S. GAAP, for both registered and non-registered funds. It focuses the financial reporting requirements under U.S. GAAP that are unique to investment companies. This online course covers the following topics: statement of assets and liabilities, statement of net assets, schedule of investments, statement of operations, statement of changes in net assets, statement of cash flows, financial highlights, special considerations for different capital structures. A final case study provides you with an opportunity to apply what you’ve learned to identify errors in an example set of financial statements. This case study is a “choose your own adventure” where you can choose whether to identify errors in the financial statements of a registered investment company or a non-registered investment company. Differences in financial reporting requirements between U.S. GAAP and IFRS are also highlighted.

We’ve bundled all these eLearning courses into a US GAAP investment management industry fundamental course collection for big savings!

U.S. GAAP Update: Investment Management (2024) – The investment management (IM) industry is unique. Therefore, your annual IM training should be too! In this CPE-eligible, eLearning course (2.0 CPE), we cover the latest developments in U.S. GAAP related to the various funds and other players that make up the IM industry, including hot topics in accounting and reporting related to the industry. If you’re a financial preparer or an auditor of funds reporting under U.S. GAAP, this online course is for you!

Liquidation Basis and Going Concern Assessment – Master the intricacies of ASC 205 with this Liquidation Basis of Accounting CPE course (1.5 CPE). This course equips accountants and auditors with the knowledge to navigate the end-of-life reporting requirements for entities under U.S. GAAP. ASC 205 addresses two key areas: the liquidation basis of accounting and the assessment of an entity’s ability to continue as a going concern. While both focus on the financial health and lifespan of an entity, they involve distinct and separate analyses. This course provides a deep dive into the liquidation basis of accounting as outlined in ASC 205-30. Learn when this accounting method is applicable, how to apply it, and the financial statement presentation and disclosure requirements involved. The course places special emphasis on challenges faced by funds in the investment management industry, a sector often characterized by entities with a defined lifespan. In addition, this course covers going concern assessments and related disclosure requirements under ASC 205-40 for situations where the liquidation basis of accounting is not applicable. Key considerations and areas of judgment are brought to life through practical examples.

Crypto Assets and the Investment Management Industry – Dive into the world of cryptocurrency accounting with this CPE-eligible (1.5 CPE) accounting for cryptocurrency CPE course, designed to equip accounting and audit professionals with the knowledge to navigate this rapidly evolving asset class. Bitcoin, launched in 2009, remains the most widely held cryptocurrency, boasting a market capitalization of over $2 trillion at the time of this course’s publication. Despite its prominence, it took the FASB 14 years to release accounting guidance (ASU 2023-08), which becomes effective in 2025. This engaging eLearning course begins with an introduction to crypto assets, offering examples and a discussion of their classification under U.S. GAAP. You’ll explore the accounting for cryptocurrency and disclosure of crypto assets as defined in ASC 350-60. Additionally, the course covers specialized accounting for investment companies under ASC 946, highlighting the interplay between ASC 350-60 and ASC 946 for entities managing crypto assets. If your organization or clients hold crypto assets, this accounting for cryptocurrency CPE course provides the insights you need to understand their accounting and disclosure requirements.

Fair Value: Hierarchy Issues – One of the main disclosure requirements of ASC 820 Fair Value Measurements is the fair value hierarchy. Such disclosures help users of the financial statements understand the inputs used to measure the fair value of financial instruments. In this CPE-eligible, microlearning course (0.2 CPE), we discuss the fair value hierarchy implications of “off-the-run” U.S. Treasury bonds, bonds priced using matrix pricing, and centrally-cleared derivatives.

Fair value: Restrictions on the Sale of Assets – How should fair value be applied to assets whose sale is restricted? After reviewing the definition of fair value and the requirement within ASC 820 to consider market participant assumptions, this CPE-eligible, microlearning course (0.2 CPE) presents a case study focused on determining whether a restriction is “entity-specific” or “security-specific.”

ASC 946: Definition of an Investment Company – Investment companies are unique, and so is their accounting. But what types of entities qualify as investment companies? This CPE-eligible, microlearning course (0.2 CPE) begins with an overview of the fundamental and typical characteristics found with ASC 946 Financial Services – Investment Companies. Then, using this information, learners are given a chance to apply what they’ve learned with a series of class examples where they must determine whether an entity is an investment company based on case facts.

ASC 946: Considerations for the Schedule of Investments – As you may recall, Investment companies have unique financial reporting requirements under ASC 946. This course focuses on one of those unique requirements, the Schedule of Investments (SOI), which must be presented when a statement of assets and liabilities is presented. In this CPE-eligible nano learning, you’ll explore the requirements for the SOI for both registered and non-registered funds.

Investment Companies: Accounting for Investments in Fixed Income Securities – Investment companies have special accounting rules that require them to account for most investments they hold at fair value with changes in fair value recorded in profit or loss. But how does this model apply to fixed income securities? What if those fixed income securities are not of a “high credit quality” when purchased? If you’re looking for a quick and fun way to learn about how an investment company accounts for fixed income securities including those that are not “of a high credit quality”, all while earning CPE, this course is for you!

In addition to these courses specific to the investment management industry, we offer additional courses on various U.S. GAAP and IFRS topics, some of which may apply to funds from time to time.

Accounting resources

CPE-eligible playback: Investment Management Hot Topics

In this conversational and scenario-based course (1 CPE), we discuss some of the hot topics, amendments, and practice issues impacting investment companies’ accounting and reporting under U.S. GAAP and ASC Topic 946. Register now!

Investment Management (ASC 946) Microlearning

Investment companies are unique…and so is their accounting! Finding high-quality, engaging, and relevant training on ASC 946 is hard! No worries. We’ve got you covered! Sample a few of our ASC 946 microlearning courses for FREE! Although we can’t issue CPE for these courses, you’ll still get the same great content.

Other resources

In addition, we have written several blogs on a variety of topics frequently encountered by the investment management industry, which are listed below. Click on the links to view the full blog post.

Accounting for Investment Companies under ASC 946: An Overview

This blog post provides an overview of our Investment Management Industry Fundamentals eLearning course collection, summarizing each of the courses and what is covered.

It’s Not Always Easy to Look Through a Fund of Funds

Preparing a Schedule of Investments for a fund-of-funds requires extra considerations, including whether the fund-of-funds needs to “look-through” its investee funds at the individual investments they hold. This blog addresses this unique requirement under ASC 946.

Investment Companies are Special… So is their Accounting!

This post highlights the unique industry that is investment management and some of the key accounting and reporting differences from traditional companies.

Readily Determinable Fair Value: Updates and The Use of Net Asset Value

Using NAV as a practical expedient to fair value is common in the investment management industry, however, it is only allowed under U.S. GAAP if certain criteria are met. One of these criteria is that the investee fund does not have a readily determinable fair value. This post discusses exactly what that means.

ASC 946: Accounting for Perpetual Debt by Investment Companies

Investment companies have special accounting under ASC 946. This post discusses the accounting for perpetual debt by investment companies.

Cryptocurrency Accounting for Investment Funds: U.S. GAAP vs. IFRS

Cryptocurrencies are becoming more and more prevalent, particularly in the investment management industry. But how are they accounted for and is there a difference between U.S. GAAP and IFRS? The answer in this blog post may surprise you!

ASC 946: Distributions from an Investment

Investment funds commonly receive distributions from its investees. In this post we discuss the challenges of the accounting under ASC 946.

Trade Date versus Settlement Date

Trade date versus settlement date. Which date should be used when accounting for investment securities? Let’s find out in today’s blog post.

We publish blog posts regularly on various accounting topics and issues relevant to the investment management industry. If you want to stay updated by receiving an email notification as new blog posts are published, you can subscribe to our blog here: Subscribe to GAAPology