Accounting for Investment Companies under ASC 946

The investment management industry is unique. In fact, the Financial Accounting Standards Board (FASB) has an entire codification topic dedicated to the accounting for investment companies: ASC 946, Financial Services – Investment Companies. Bob covered some of those unique accounting rules this blog post, but that post really just scratches the surface of the differences between accounting for an investment company and accounting for a more traditionally structured entity! Those working in the investment management industry, or responsible for auditing companies operating in this space, know that finding high-quality, easy to understand accounting training on the requirements of ASC 946 is next to impossible! This post takes a deeper dive into the accounting for investment companies under ASC 946 and the related accounting and reporting issues.

Investment company (ASC 946) CPE training

For over ten years, GAAP Dynamics has provided specialized training in this industry, traditionally offered as an instructor-led training (ILT) at our clients’ location. In response to the lack of high-quality CPE-eligible eLearning on Investment Company accounting under U.S. GAAP, Bob Laffler and Chris Brundrett put their heads together to create the Investment Management Industry Fundamentals (IMIF) eLearning course collection – a collection of 9 eLearning courses worth a total of 10.9 CPE. And with GAAP rock stars like Bob and Chris at the helm, you know it’s going to be an informative AND fun ride!

Let’s take a closer look at some of the guidance related to the accounting for investment companies covered in each of these courses.

1. Industry overview (1.0 CPE)

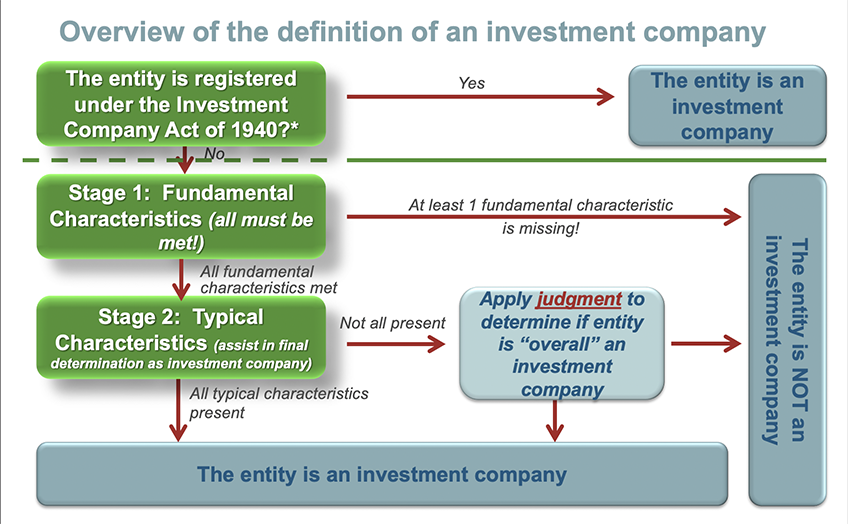

This course presents an overview of the investment management industry and serves as an introduction to the applicable accounting guidance for investment companies. One of the key concepts you’ll learn includes the definition of an investment company, which is crucial in determining whether or not you need to apply the guidance in ASC 946!

An entity that is registered under, and therefore regulated by, the Security and Exchange Commission’s Investment Company Act of 1940 automatically meets the definition of an investment company. No further analysis is required.

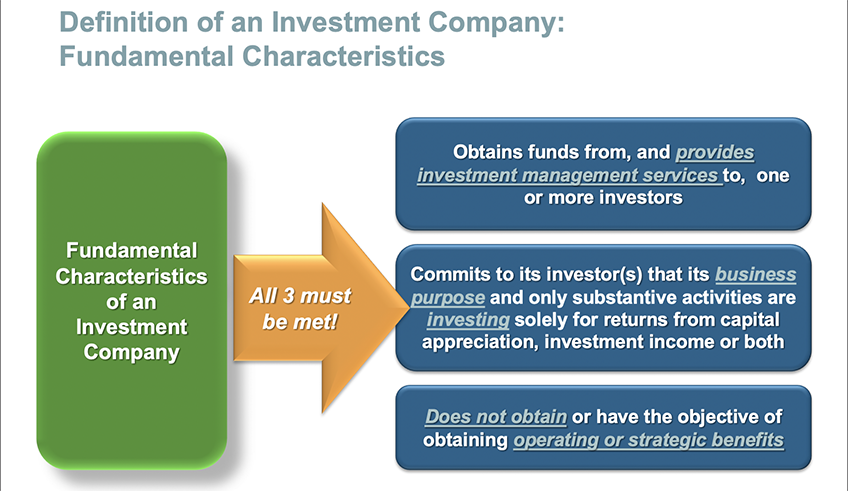

For entities that are not registered with the SEC, further analysis is required under a two-stage approach. The first stage looks at specific characteristics deemed by the FASB as “fundamental” for an investment company.

An entity that is missing even one of those fundamental characteristics is NOT an investment company. Even if an entity has all the fundamental characteristics, further analysis is still required in stage 2. In stage 2, “typical” characteristics of an investment company are considered. If an entity has all of the typical characteristics, as defined by the FASB, then the entity is an investment company. In short, all the fundamental characteristics, plus all of the typical characteristics, means the entity is an investment company. If all of the typical characteristics are not present, then judgment must be applied to determine whether or not the entity is an investment company.

In addition to the definition of an investment company in U.S. GAAP, the following topics are also discussed:

- Characteristics of an investment company

- Investment strategies

- General categories

- Capital and legal structures

- Key players (service providers)

- Overview of applicable U.S. GAAP accounting guidance

This course is a must for anyone beginning to work in the investment management industry and serves as the backbone of the Investment Management Industry Fundamentals learning path!

2. Investments (2.0 CPE)

Investments can take many different shapes within investment companies: equity securities, debt securities, derivative instruments, real estate, commodities, even collectibles, such as rare artwork. Investments are crucial as this is the primary purpose of an investment company and the primary way these companies earn a return on investment.

According to the guidance in ASC 946, all investments are measured at fair value with changes in fair value recognized through the Statement of Operations (this is an investment company’s equivalent of an income statement…more on that later) – this is generally true regardless of the classification of the investment as debt or equity or some other form of investment!

Seems simple and consistent enough, but are there other issues worth mentioning? You better believe it! ASC 946 provides some specific guidelines when it comes to the initial measurement of investments, for example:

- The timing of initial recognition – ASC 946 requires investment companies to account for purchases and sales of investments on the trade date (the date in which the order to purchase the investment is placed, typically with a broker)

- The treatment of transaction costs – While the definition of fair value under ASC 820 clearly states that transactions costs are generally omitted from a fair value measurement and recognized through expense as incurred, investment companies under ASC Topic 946 have specific guidance regarding initial measurement and subsequent measurement, resulting in a unique way these costs are presented

In particular, this course focuses on the accounting and reporting for investments, including:

- The timing of recognition and the treatment of initial costs

- The most common types of investments held by an investment company, including:

- Equity securities

- Debt securities

- Alternative investments

- Investments in other investment companies

- How investment income is derived from these investments and recognized in the financial statements

3. Fair Value: Overview of ASC 820 (1.5 CPE)

Now that you’ve learned that all investments held by an investment company are measured at fair value through the statement of operations, it is time to learn what fair value means in accordance with ASC 820 and how it can be determined for various types of investments.

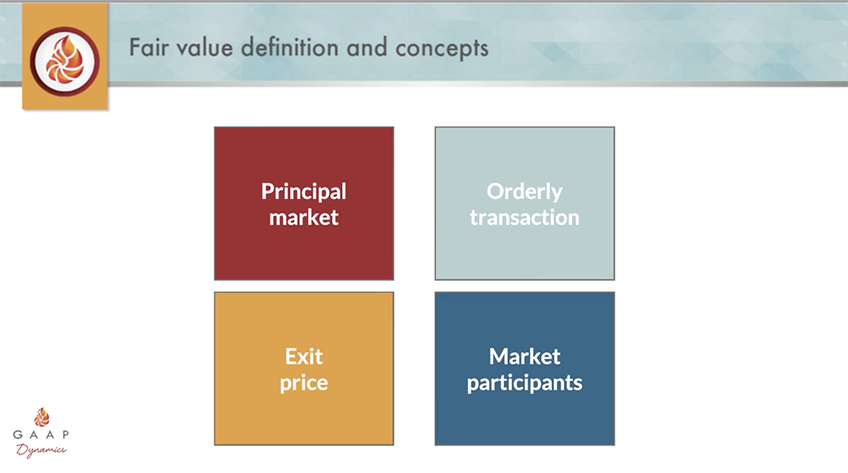

Fair value is the price that would be received to sell an asset or paid to transfer a liability in an orderly transaction between market participants at the measurement date. There are four main concepts incorporated into this fair value definition, which are addressed in the training:

- Where the transaction takes place

Fair value measurements assume that the transaction to sell the asset or transfer the liability occurs in the principal market or, in its absence, the most advantageous market. The principal market is the market with the greatest volume and level of activity that can be accessed by the entity selling the asset or transferring the liability. The most advantageous market is the market that maximizes the amount that would be received to sell an asset (or minimizes the amount that would be paid to transfer a liability), after taking into account transaction and transportation costs.

- The price

Fair value is the price that would be received to sell an asset or paid to transfer a liability, which represents an exit price notion. By comparison, an entry price is the price paid to acquire an asset or received to assume a liability in an exchange transaction. While an exit and an entry price may be identical in many situations, this may not always be the case. Therefore, it is important to remember the entry price does not represent the fair value of an asset or liability.

- The orderliness of the transaction

An orderly transaction is a transaction that assumes exposure to the market for a period before the measurement date. This period allows for marketing activities that are usual and customary for transactions involving such assets or liabilities to take place and be reflected in the market price. An orderly transaction is not a forced transaction (e.g. a forced liquidation or a distressed sale). Rather, it’s a mutual coming together of a willing buyer and seller.

- Market participants

Market participants are the buyers of assets or assumers of liabilities in the exit market (principal or most advantageous). While identifying the market participants for an actively traded equity security may seem straightforward, identifying the market participants of a non-financial asset or liability often requires judgment. Why does it matter? Identifying the market participants for the asset or liability being valued is important because all of the assumptions that are used in that valuation should be from the market participant’s perspective.

As you’re probably imagining, there are several issues that commonly crop up in the investment management industry when measuring investments at fair value, including determining whether a transaction is orderly, which is the principal market, and correctly identifying market participants.

After a review of the various balance sheet items which utilize fair value measurements, the course explores key concepts of fair value: Utilizing market participant assumptions; distinguishing between orderly transactions versus forced transactions; using exit prices and not entry prices; and determining the principal market. The course then discusses the various approaches to determine fair value measurements, including the importance of inputs and their classification within the fair value hierarchy. The course concludes with a look at “real-life” fair value disclosures, highlighting the requirements within ASC 820.

4. Fair value: Advanced issues (1.5 CPE)

Now that you know the basics of fair value, it is time to take it to the next level. This course begins with a discussion on active, inactive, and disorderly markets, and their impact on fair value measurement. These all represent issues that investment companies frequently face in practice!

It then provides the learner with an in-depth understanding of using net asset value (NAV) as a practical expedient to fair value, including the requirements for use and when it may no longer be acceptable. NAV per share is the amount of net assets attributable to each outstanding share of an investment at the close of a period. The NAV per share of any portfolio of pooled securities, including mutual funds, hedge funds, or private funds, is the sum of its assets minus its liabilities, divided by the number of shares outstanding.

Certain funds (e.g. mutual funds) calculate NAV per share once per day based on the closing market prices of the investments held within a fund’s portfolio. Hedge funds and private funds will likely calculate NAV per share less frequently (e.g. monthly or quarterly). Funds also may issue financial statements to their investors that report the calculated NAV per share or unit on a daily, monthly, quarterly, or annual basis.

The FASB permits, but does not require, the use of NAV per share as a practical expedient for fair value if certain conditions are met. Investors may use NAV per share to estimate the fair value of investments if:

- The investment does not have a readily determinable fair value

- The investment is in an investment company within the scope of ASC Topic 946 or is an investment in a real estate fund for which it is industry practice to measure investment assets at fair value on a recurring basis and to issue financial statements that are consistent with the measurement principles in ASC Topic 946

- And, the NAV per share is calculated consistent with the measurement principles of ASC Topic 946 as of the measurement date

If the NAV per share of the investment obtained from the investee is not as of the reporting entity’s measurement date or is not calculated in a manner consistent with the measurement principles of ASC 946, the reporting entity may need to adjust the most recent NAV per share. It is also important to note that NAV per share is not always representative of fair value as defined by ASC Topic 820.

The course ends with an overview of determining the fair value of liabilities and advanced issues applicable to categorizing fair value measurements as either level 1, level 2, or level 3 within the fair value hierarchy.

5. Fair value: Hierarchy issues (0.2 CPE)

One of the main disclosure requirements of ASC 820 Fair Value Measurements is the fair value hierarchy. Such disclosures help users of the financial statements understand the inputs used to measure the fair value of financial instruments. In this CPE-eligible, microlearning course (0.2 CPE), we discuss the fair value hierarchy implications of “off-the-run” U.S. Treasury bonds, bonds priced using matrix pricing, and centrally-cleared derivatives.

6. Fair value: Restrictions on the sale of assets (0.2 CPE)

What happens if an investment company holds an asset that has a restriction on sale? When measuring fair value should that discount be included in the fair value measurement of that restricted investment. Well, it depends! This microlearning course walks through when and when you should not include restrictions on sale in the fair value measurement of an investment.

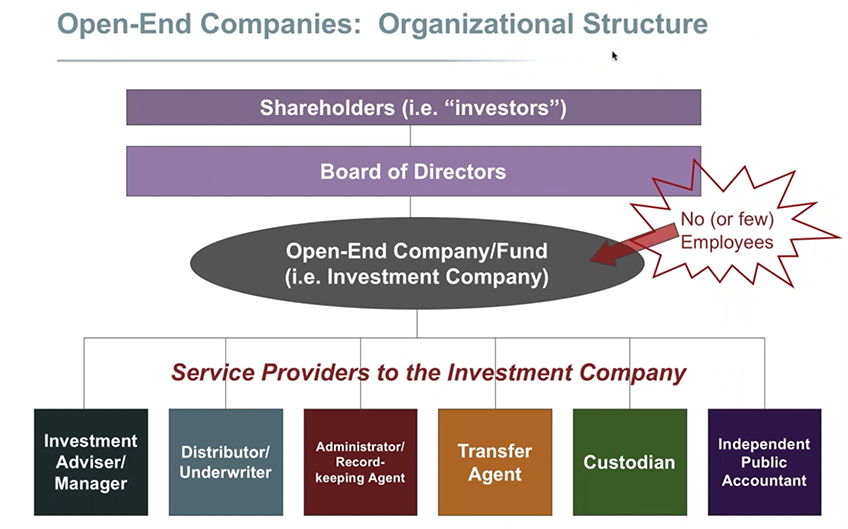

7. Transactions with service providers (1.5 CPE)

Now that you’ve taken a look at how an investment company makes its money (through investments) and how to measure those investments at fair value, it’s time to take a look at some of the expenses that impact an investment company’s statement of operation: transactions with service providers.

This course explains who the typical service providers of an investment company are, including:

- Investment advisers

- Distributors and underwriters

- Administrators and record-keeping agents

- Transfer agents

- Custodians

- And even the public accountant!

After reviewing the role each service provider plays, you’ll look at how they are compensated, highlighting the fact that most of the functions of an investment company are performed by these service providers. Typical fee arrangements are covered, with particular focus on the management fee and distribution fee. For example, management fees will generally be recognized based on actual performance through the accrual date. This calculation may be daily, monthly, quarterly, or annually depending on how often shares are bought and sold.

Fee waiver, reimbursement and expense offset arrangements are discussed along with their presentation in the financial statements. You’ll explore these concepts and more with Bob Laffer and Chris Brundrett offering plenty of examples and journal entries along the way to help bring the accounting to life.

8. Transactions with unit holders (1.5 CPE)

Now that we’ve covered how an investment company makes money, and what expenses it incurs, this course describes how capital share transactions are accounted for by an investment company along with the accounting for other fees incurred by unit holders related to capital share transactions. In addition, the common capital structures utilized by investment companies will be discussed including the key impacts those structures have on the financial statements, including:

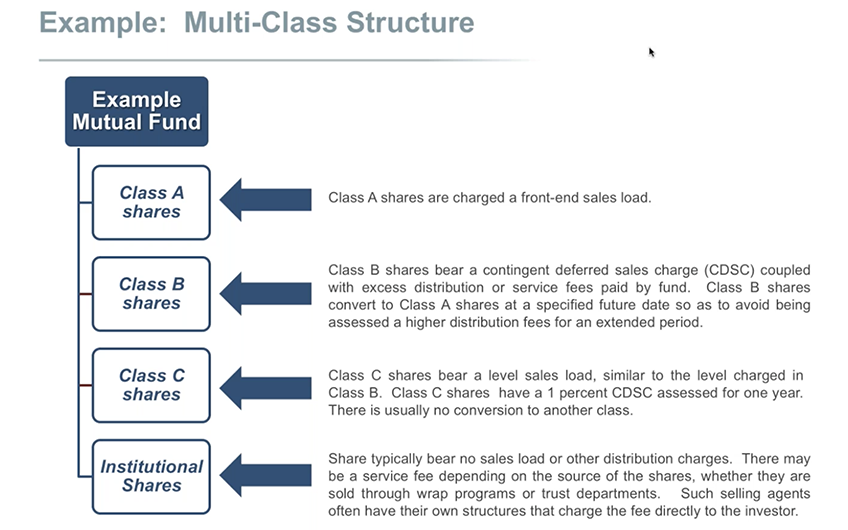

Multi-class structures are those funds that issue more than one class of shares. These classes are often distinguished by different kinds of sales charges, different charges to classes of shares for specific expenses, or even can be differentiated by different currencies. Income, expenses, gains and losses are allocated to each share class. Fees and expenses can either be class-level, and applied directly to the class to which they relate, or fund-level, and allocated across the share classes. Calculation and distribution of dividends and the calculation of investment performance is also done on a per class basis.

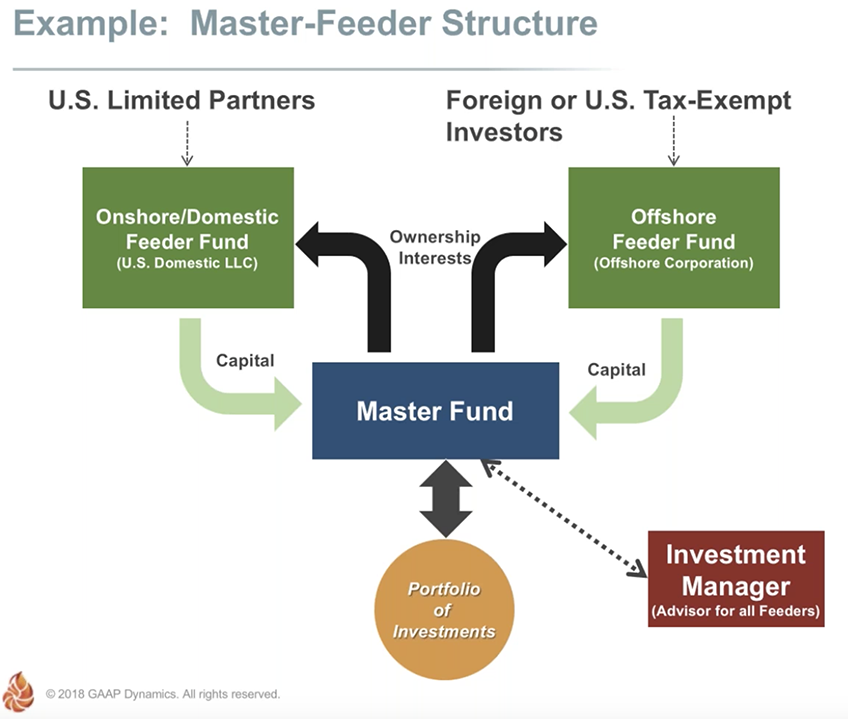

A master-feeder structure, like the one shown, is often used to provide offshore investors, who are U.S. Tax Exempt investors, access to funds without having to worry about U.S. Tax implications. In these scenarios, a Master Fund is established which holds the portfolio of investments and works directly with the investment manager. The Master Fund then establishes ownership interest in two feeder funds, the Onshore Fund and the Offshore Fund, in this example. Investors invest directly into the Onshore or Offshore funds, depending on their location, and the Onshore and Offshore funds then invest exclusively in the Master Fund.

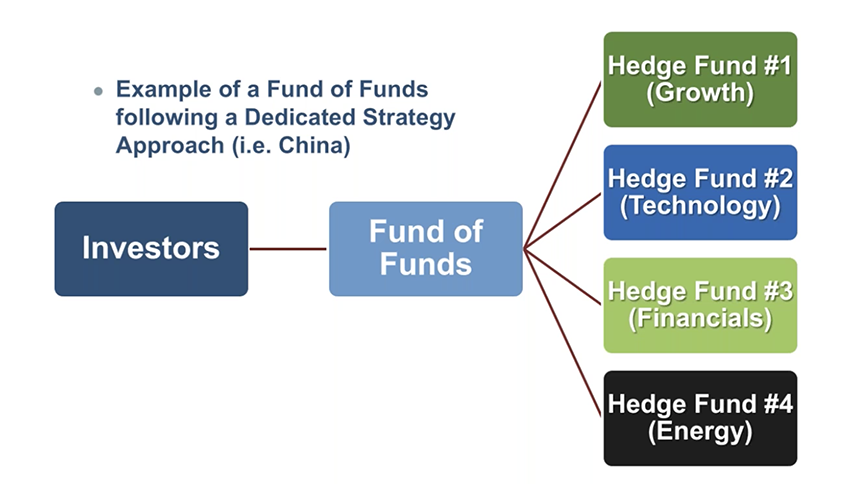

In this structure, the investment company primarily holds its investments solely or primarily in other investment companies. In other words, the investment company is a fund that invests in other funds. This type of fund structure enhances diversification and allows common investors to invest in exclusive funds that otherwise require too large of an investment.

9. Financial reporting (1.5 CPE)

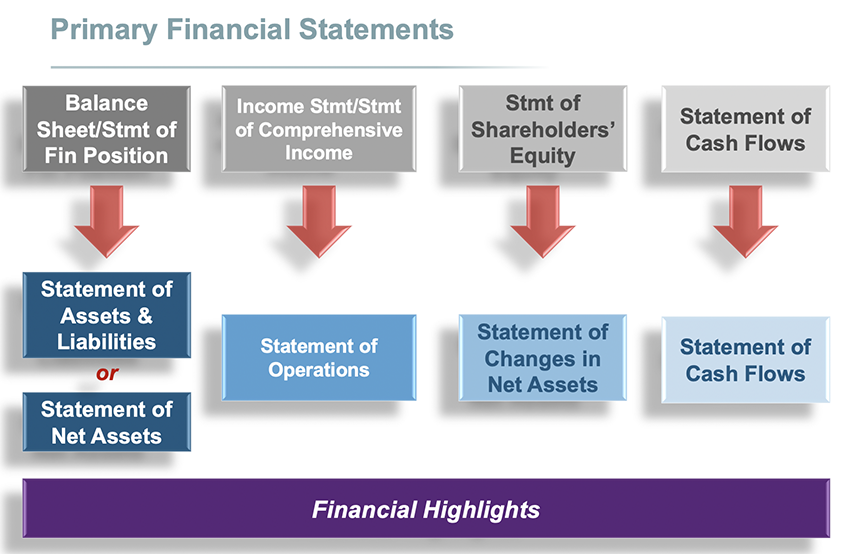

This course explains the financial reporting requirements for investment companies under U.S. GAAP, both registered and non-registered. You’ve already seen that the accounting for investment companies is unique, but so too are their financial reporting requirements! As you can see, the financial statements even have different names.

Particular focus is on the requirements that are unique to investment companies. Topics covered include:

- Statement of assets and liabilities

- Statement of net assets

- Schedule of investments

- Statement of operations

- Statement of changes in net assets

- Statement of cash flows

- Financial highlights

- Special considerations for different capital structures

A final case study provides the learner with an opportunity to apply their knowledge to identify errors in an example set of financial statements. This case study will be a “choose your own adventure” where the learner can choose whether to identify errors in the financial statements of a registered investment company or a non-registered investment company.

Differences in financial reporting requirements between U.S. GAAP and IFRS will be highlighted.

Final thoughts

Well that’s it! We hope this post has helped you with understanding the accounting for investment companies in accordance with ASC 946 and the main accounting and reporting issues associated with these entities. If you need ASC 946 training, check out our Investment Management Industry Fundamentals (IMIF) eLearning courses or contact us to discuss a tailored, live training option for your team!

About GAAP Dynamics

We’re a DIFFERENT type of accounting training firm. We view training as an opportunity to empower professionals to make informed decisions at the right time. Whether it’s U.S. GAAP, IFRS, or audit training, we’ve trained thousands of professionals since 2001, including at some of the world’s largest firms. Our promise: Accurate, relevant, engaging, and fun training. Want to know how GAAP Dynamics can help you? Let’s talk!

Disclaimer

This post is for informational purposes only and should not be relied upon as official accounting guidance. While we’ve ensured accuracy as of the publishing date, standards evolve. Please consult a professional for specific advice.