IFRS 16 vs ASC 842: How to Account for Low-Value Leases

IFRS 16 and ASC 842 require entities to recognize (most) leases on the balance sheet. I say most, because all accounting guidance generally allows for certain exceptions, depending on the topic! A common question asked by entities upon adopting IFRS 16 and ASC 842 centered around the threshold of leases requiring recognition. For example, entities asked about leases relating to low-value items or short-term leases.

This post looks to each standard, IFRS 16 and ASC 842, to evaluate the requirements relating to low-value leases.

Low-value lease scenario

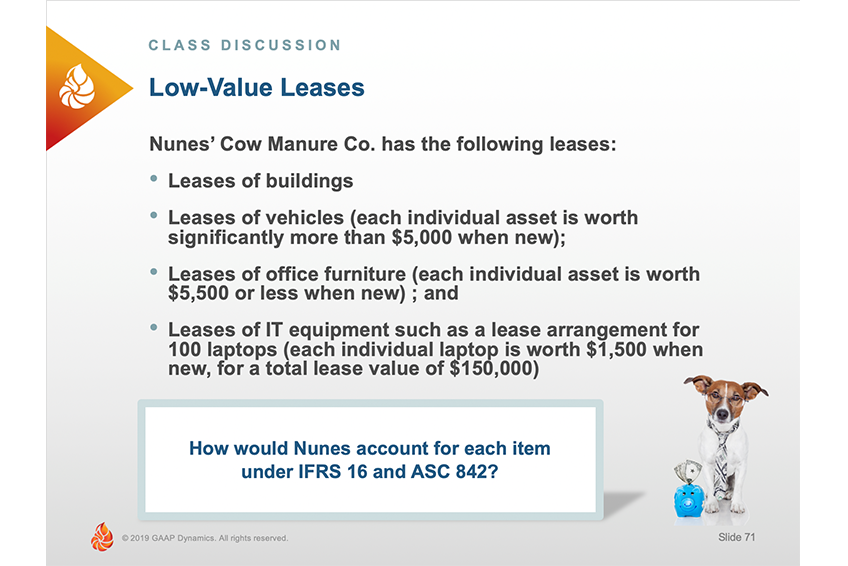

Let’s use an example to help illustrate IFRS 16 and ASC 842 requirements. Consider the following case facts about Nunes’ Cow Manure Company.

Note: These case facts are based off of the fact pattern discussed by the Canadian Accounting Standards Board’s IFRS Discussion Group.

IFRS 16

IFRS 16 requires all leases to be recognized on the balance sheet, but it allows for two exemptions:

- Short-term leases

- Low-value leases

Both the IASB and the FASB define short-term leases as those whose term is one-year or less. Based on the case facts for Nunes’ Cow Manure Co., there is nothing that would suggest that any of these leases would qualify for the short-term exemption. For more information on determining the lease term, make sure to check out this blog post.

This leads us to the second exemption: low-value leases. IFRS 16 provides lessees with an election not to recognize a right-of-use asset and lease liability for leases for which the underlying asset is of low value. Here are some of the key considerations when determining whether or not a lease qualifies for this exemption:

- “Low-value” is generally meant to mean $5,000 or less (note that this is not explicitly stated in the standard, but instead mentioned in the Basis for Conclusions of IFRS 16)

- The underlying value of the asset is based on the value of the asset when it is new, even if the asset being leased is not new

- The election is made on a lease-by-lease basis

- The asset can only be low value if:

- The lessee can benefit from the use of the underlying asset on its own or together with other resources that are readily available

- The underlying asset is not highly dependent on, or highly interrelated with, other assets

So, which of the leases mentioned in the case facts can qualify for the exemption?

Leases of buildings

While we don’t know the specifics, I believe it is safe to assume that this would NOT qualify for the low-value lease exemption and, therefore, should be recorded as a right-of-use asset and lease liability on the balance sheet.

Leases of vehicles

Again, because the case facts state that the asset value is clearly above $5,000 when new, these leases would not qualify for the exemption under IFRS 16.

Leases of office furniture

Here, the answer likely depends on how you interpret the guidance above. Most specifically, how you interpret the IASB’s response in its Basis for Conclusion that states that “low-value” is meant to be assets worth $5,000 or less. If you conclude this amount is not intended to be a bright-line test, then perhaps the leases of office furniture could be considered low-value and qualify for the exemption. Even if you do interpret the “$5,000 or less” as a bright-line test, remember, each lease should be evaluated individually. So, those pieces of office furniture whose values are less than $5,000 could be considered low-value and exempted from recognition.

Leases of IT equipment

For this scenario, it likely depends on how an entity views the “lease-by-lease basis” criterion. The leases for each of these individual laptops was entered into in one arrangement. So, if the entity considers this arrangement as a whole, the value exceeds the $5,000 threshold, and so recognition of the right-of-use asset and lease liability would be required. However, the entity could also argue that each of those laptops represents an individual lease arrangement and the value is clearly below the $5,000 threshold, thereby qualifying for the recognition exemption.

ASC 842

ASC 842 does NOT have the same low-value lease recognition exemption that IFRS 16 has. In fact, the ONLY exemption provided by ASC 842 is for short-term leases.

Therefore, the “correct” answer under ASC 842 is that all of Nunes’ Cow Manure’s leases would need to be recognized on the balance sheet, regardless of the value of the underlying assets!

However, in practice, we expect that many entities will utilize something similar to their PP&E capitalization policies when determining whether to recognize a lease or not. But BEWARE! This is a non-GAAP policy! This means that an entity will need to be able to document and prove to its auditors that the right-of-use assets and lease liabilities not recognized are immaterial, individually and in the aggregate, to the financial statements!

Final thoughts

There are so many components and requirements when it comes to accounting for leases under both IFRS 16 and ASC 842. Check out our Leases Topic Page for important considerations. Also check out our ASC 842 course collection or our course collection on IFRS 16.

About GAAP Dynamics

We’re a DIFFERENT type of accounting training firm. We view training as an opportunity to empower professionals to make informed decisions at the right time. Whether it’s U.S. GAAP, IFRS, or audit training, we’ve trained thousands of professionals since 2001, including at some of the world’s largest firms. Our promise: Accurate, relevant, engaging, and fun training. Want to know how GAAP Dynamics can help you? Let’s talk!

Disclaimer

This post is for informational purposes only and should not be relied upon as official accounting guidance. While we’ve ensured accuracy as of the publishing date, standards evolve. Please consult a professional for specific advice.