Transfer Troubles: Sale or Secured Borrowing under ASC 860?

Repurchase agreements, securitizations, and loan participations are all common transactions executed by banks. Unfortunately, these common transactions can be quite the source of “trouble,” as they involve the transfer of financial assets. ASC 860, Transfers and Servicing provides detailed guidance regarding the accounting treatment for the transfers of financial asset(s). This post explores common transfers by banks that are within the scope of ASC 860, discusses why transfers can be a troublesome area, and helps you determine whether a transfer is it a sale or secured borrowing under ASC 860. This post is at a high-level, but don’t worry. If you need more in-depth training on this tricky topic, check out our Transfers of Financial Assets eLearning course!

What exactly is a transfer under ASC 860?

ASC 860, Transfers and Servicing defines a transfer as “the conveyance of a non cash financial asset by and to someone other than the issuer of the financial asset.” Notice that the definition specifically notes that neither of the two parties involved are the issuer of the financial asset. This means that originations, redemptions, modifications, or any direct transaction with the issuer is not a transfer for the purposes of ASC 860.

Common types of transfers executed by banks that are within the scope of ASC 860 include:

- Repurchase agreements: Repos are often used by banks to obtain short-term funds by transferring collateral (i.e., securities) in exchange for cash. Upon maturity of the agreement, cash (plus interest) is returned to the lender and the collateral is returned to the borrower.

- Securitizations: These are a form of structured finance to turn individual rights to future cash flows into a security that can be easily purchased and sold. Banks commonly securitize loans.

- Participation loans: A bank will originate a loan to a borrower and subsequently (or concurrently) with the origination of this loan, the originating bank arranges a participation with another or multiple other lenders. Under the agreement, the participating bank(s) agree to assume the risks and rewards of a portion of this loan by transferring funds to the originating bank in return for the rights to cash payments for that portion of the loan participated out to the participating bank.

Other examples of transfers include securities lending transactions and factoring.

Sale or a secured borrowing?

Transactions involving the transfer of financial assets must be analyzed to determine if the transfer qualifies as a sale or a secured borrowing. This determination is critical, as it drives the accounting treatment. Sales result in the derecognition of the financial asset transferred, while secured borrowings do not result in the derecognition of the financial asset transferred.

ASC 860 provides detailed criteria for achieving derecognition. If these criteria are not met, by default, the transfer must be accounted for as a secured borrowing. The difference in accounting can have a major impact on the way an entity’s financial health is viewed by others, particularly in the banking industry.

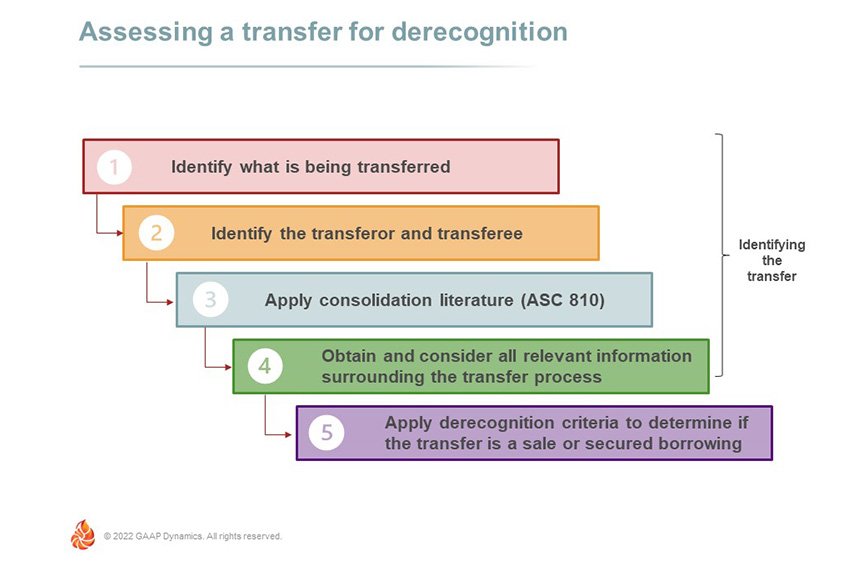

Assessing a transfer for derecognition

The determination of whether a transaction should be accounted for as a sale or a secured borrowing requires careful analysis. Here at GAAP Dynamics, we’ve found it’s easiest to make this assessment by working through the five steps shown in the image above. ASC 860 does not explicitly note these five steps, but the points addressed by each of the steps are required by the guidance.

- Step 1: Identify what’s transferred: Is the transfer an entire financial asset, a group of entire financial assets or a component of an entire financial asset?

- Step 2: Identify the transferor and transferee: The relationship between the parties involved in the transaction drives the complexity of this step, as the transferee may need to be consolidated by the transferor.

- Step 3: Apply consolidation literature: ASC 810, Consolidation is your guide here! Once all subsidiaries have been consolidated, transfers outside of the consolidated group can be analyzed for derecognition.

- Step 4: Obtain and consider all relevant information surrounding the transfer process: This step involves identifying all aspects of a transferor’s continuing involvement in the asset.

- Step 5: Apply the derecognition criteria to determine if the transfer is a sale or a secured borrowing: This step focuses on control – has the transferor surrendered control over the financial asset being transferred?

Historically, the vast majority of time is spent on step 5, however, the first three steps are essential because these steps identify and accumulate all necessary information in order to apply Step 5 properly.

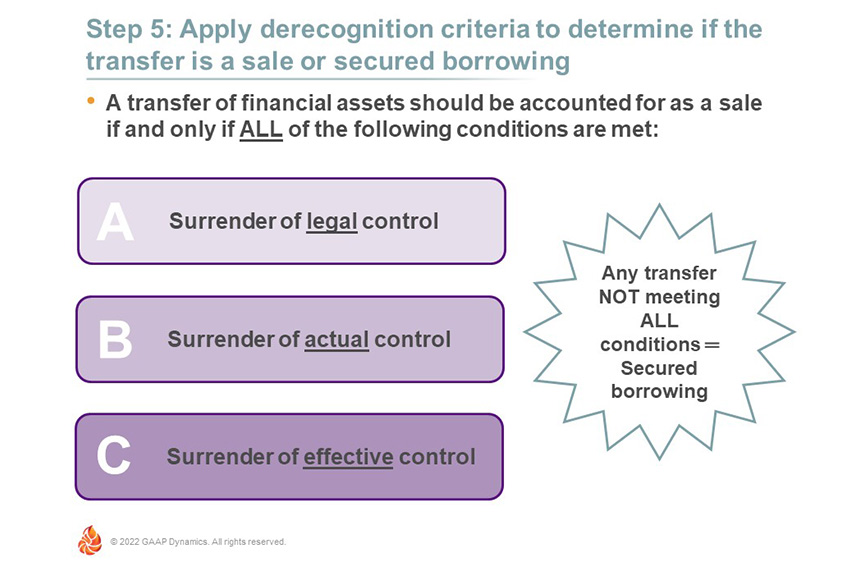

Step 5: It’s all about control!

There are three criteria required to be met to achieve derecognition of the transferred asset. These three conditions are different forms of control that must be relinquished by the transferor. If any of these three criteria are not met, the transfer does not qualify for derecognition, and the transfer must be accounted for as a secured borrowing.

A transfer of financial assets should be accounted for as a sale if, and only if, ALL of the following conditions are met:

- Surrender of legal control

- Surrender of actual control

- Surrender of effective control

Transfer agreements involving restrictions where the transferee can sell the transferred assets only on a certain date, sell only to certain entities, or right of first refusal clauses can cause this step to be complex. (Don’t worry – we cover these scenarios and more in our Transfers eLearning!)

Accounting treatment for transfers under ASC 860

The determination of whether a transfer qualifies to be accounted for as a sale or whether it must be accounted for as a secured borrowing is critical, as it drives the accounting treatment. All of the criteria in ASC 860 must be met to achieve, or qualify for, sale accounting. If any of the criteria are not met, then the transfer is required to be accounted for as a secured borrowing. As a reminder, sale treatment must be qualified for – it’s not an accounting policy election!

Transfers accounted for as sales result in the derecognition of the financial asset transferred with a corresponding gain or loss from the transaction. Secured borrowings, on the other hand, do not result in the derecognition of the financial asset transferred and therefore no gain or loss is recognized.

Closing thoughts

As mentioned at the onset, transfers is a source of troubles for banks and other financial institutions. For more training on transfers and other banking-related topics, check out our Banking Industry Fundamentals and Advanced Banking Industry Fundamentals course collections. Want a live, tailored training for your organization? We do that too!

About GAAP Dynamics

We’re a DIFFERENT type of accounting training firm. We view training as an opportunity to empower professionals to make informed decisions at the right time. Whether it’s U.S. GAAP, IFRS, or audit training, we’ve trained thousands of professionals since 2001, including at some of the world’s largest firms. Our promise: Accurate, relevant, engaging, and fun training. Want to know how GAAP Dynamics can help you? Let’s talk!

Disclaimer

This post is for informational purposes only and should not be relied upon as official accounting guidance. While we’ve ensured accuracy as of the publishing date, standards evolve. Please consult a professional for specific advice.