SAS 145 requires auditors to “stand-back” and assess material transactions, accounts, and disclosures that haven’t been deemed as significant. Read More ...

SAS 145 requires auditors to “stand-back” and assess material transactions, accounts, and disclosures that haven’t been deemed as significant. Read More ...

Issues in the banking industry have left many asking “why?” Why did this happen, why were investments transferred, and why is this allowed under ASC 320, Debt Securities? Read More ...

Some cars now require software updates. How are these accounted for? This post covers Tesla cars, software updates, and ASC 606, Revenue Recognition. Read More ...

The interest method is used throughout U.S. GAAP. This post explores our CPE-eligible, eLearning course: Interest Method and Effective Interest Rates. Read More ...

Looking for a training solution that connects key audit concepts with your firm’s specific audit approach? New Cornerstones of Audit courses are here! Read More ...

ASU 2022-02 eliminates the accounting guidance for troubled debt restructurings (TDRs) by creditors; however, it also enhances disclosure requirements. Read More ...

Reports have been released for firms annually inspected by the PCAOB. This post explores the results of the 2020 PCAOB inspection cycle. Read More ...

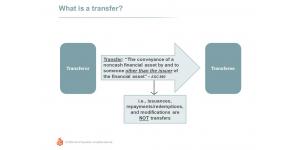

Determining if a transfer is a sale or secured borrowing under ASC 860 can be a source of trouble for banks! This post discusses key guidance. Read More ...

Cookies on the GAAP Dynamics website

To give you the best possible experience, this website uses cookies. By continuing to browse this website you are agreeing to our use of cookies. For more details about cookies and how to manage them, please see our privacy policy.